We’re revealing exclusive data from 2025, based on our $950M+ in listings, analyzing the most in-demand brands and watch styles, the prevalence of inauthentic watches on the secondary market, and Bezel's unending commitment to refining the luxury watch-buying experience.

Welcome to the 2025 Bezel Report! This is our time to analyze a full year’s worth of transactional and behavioral data from the Bezel platform: thousands of purchases, millions of user interactions, and almost a billion dollars in active listings.

Since the last report, we’ve seen tariffs rock the watch market, new insights coming from the launch of Bezel Insurance, and a meaningful increase in data driven by our rapid growth.

At Bezel, our goal has stayed consistent: offering the most trusted platform for buying, selling, and collecting watches. As we continue to grow, we’re committed to consistently sharing our learnings on authentication processes, purchase behavior, market trends, consumer preferences, and more in these Bezel reports.

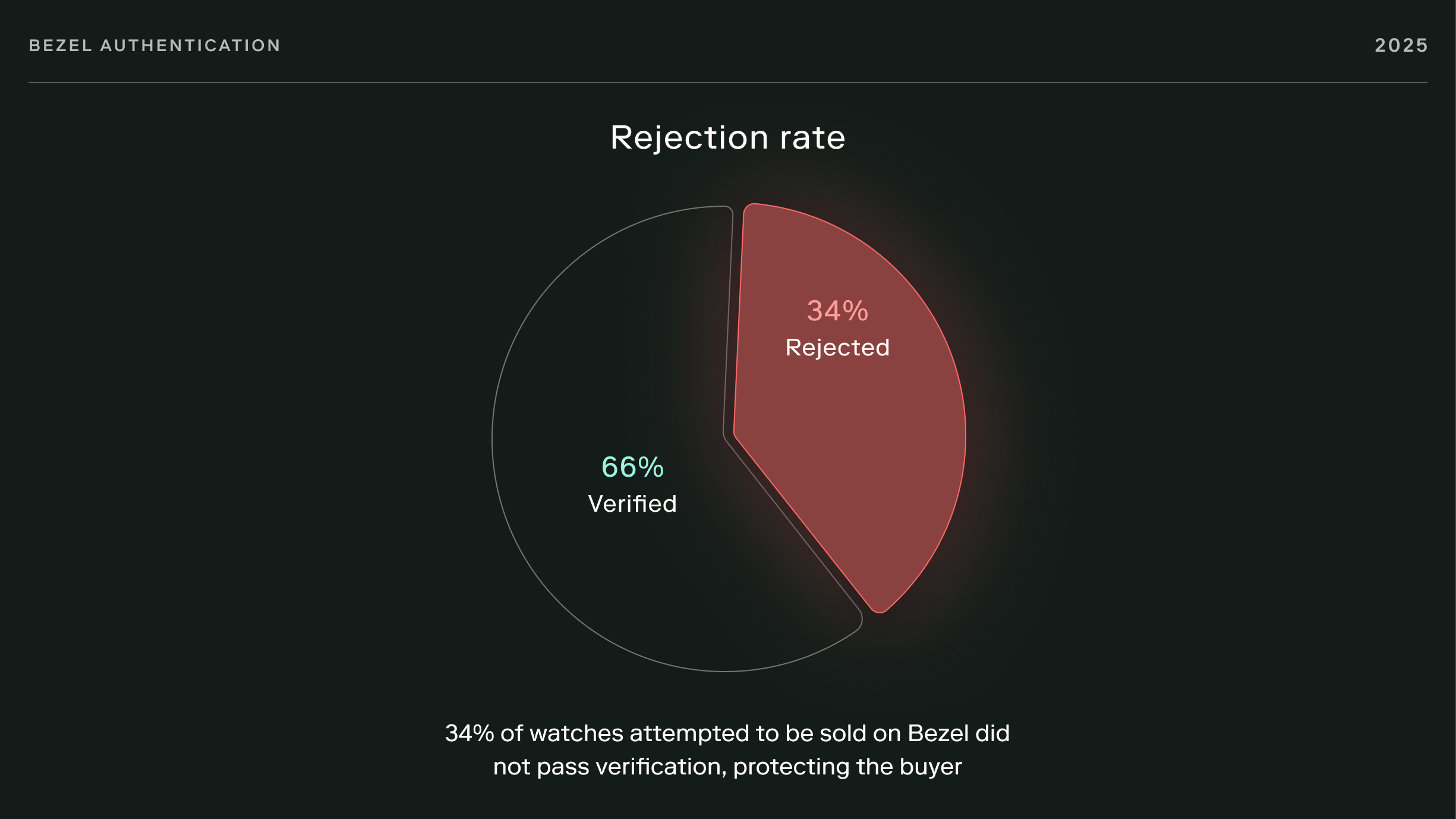

We’ll dive into the details in the report, but we rejected 38% of the listings attempted to be sold in H2, bringing the 2025 rejection rate up to 34%. As the rejection rate continues to increase, we believe it further affirms our authentication process and illustrates our commitment to building the safest place to collect.

I hope you find the data as interesting as we do. As always, please reach out to your Client Advisor (directly in the Bezel app or website) if you have any questions, thoughts, or requests for the next report.

An Introduction to the 2025 Bezel Report

Authentication & Rejection Rates in 2025

Counterfeit Papers on a Rolex Day-Date 36

A Counterfeit Cartier Tank Must XL

Mismatched Documentation on a Rolex GMT-Master II

Undisclosed Internal Wear on an Audemars Piguet CODE 11.59 Chronograph

What Bezel Clients Bought, Wanted, and Owned Throughout 2025

After several years of fast movement and speculative excess, the market entered 2025 in an unsettled state. Tariffs followed. Duties were proposed, timelines shifted, and policy direction changed more than once. The result was confusion that bled into behavior across both the primary and secondary markets. Inventory moved early. Pricing assumptions broke down. Buyers hesitated, then rushed. Sellers repriced, then paused. For much of the year, the market felt dislocated. Against that backdrop, what actually happened beneath the surface was quieter and more structural.

Prices adjusted. Supply tightened. Demand recalibrated. What emerged was not a new cycle or a clean reset, but a sorting process that separated structural value from hype, liquidity from noise, and long-term intent from short-term trade.

Bezel’s platform activity offered a clean window into how collectors behaved once the policy noise faded into the background. What people bought. What they tracked. What they chose to hold. Where transactions broke down. Where risk surfaced. And which watches continued to move when urgency dissipated.

This latest edition of the Bezel Report draws on that full picture. It combines transactional data, authentication outcomes, ownership behavior, and cultural signals to map how the market functioned in practice.

The big highlight: Bezel rejected 34% of the watches attempted to be sold in 2025. That’s a 5% increase from our 2024 Bezel Report (where we ended the year at a 29% rejection rate), and an 11% increase from 2023 (23%).

Throughout 2025, Bezel’s authentication team continued to apply the same multi-point, in-house verification standards to every watch submitted to the platform, regardless of brand, value, or origin. Across the full calendar year, 34% of watches attempted to be sold on Bezel were rejected, reflecting both the scale of activity on the secondary market and the growing complexity of inventory now circulating globally.

Rejection activity was not evenly distributed across the year. In the first half of 2025, the rejection rate stood at 27%, before climbing to 38% in the second half. Supply tightened, pricing pressure intensified, and inventory began moving more aggressively in the wake of tariff-related disruptions earlier in the year. Periods like this tend to expose weak points in the market, where inconsistencies in stated condition, undisclosed modifications, and departures from period correctness become more common.

Bezel upheld its rigorous standards during these conditions. With less inventory available and deals moving faster, issues surfaced that tend to slip through in less controlled environments. That rise in rejections reflects Bezel’s insistence on applying the same verification criteria as pressure built across the market.

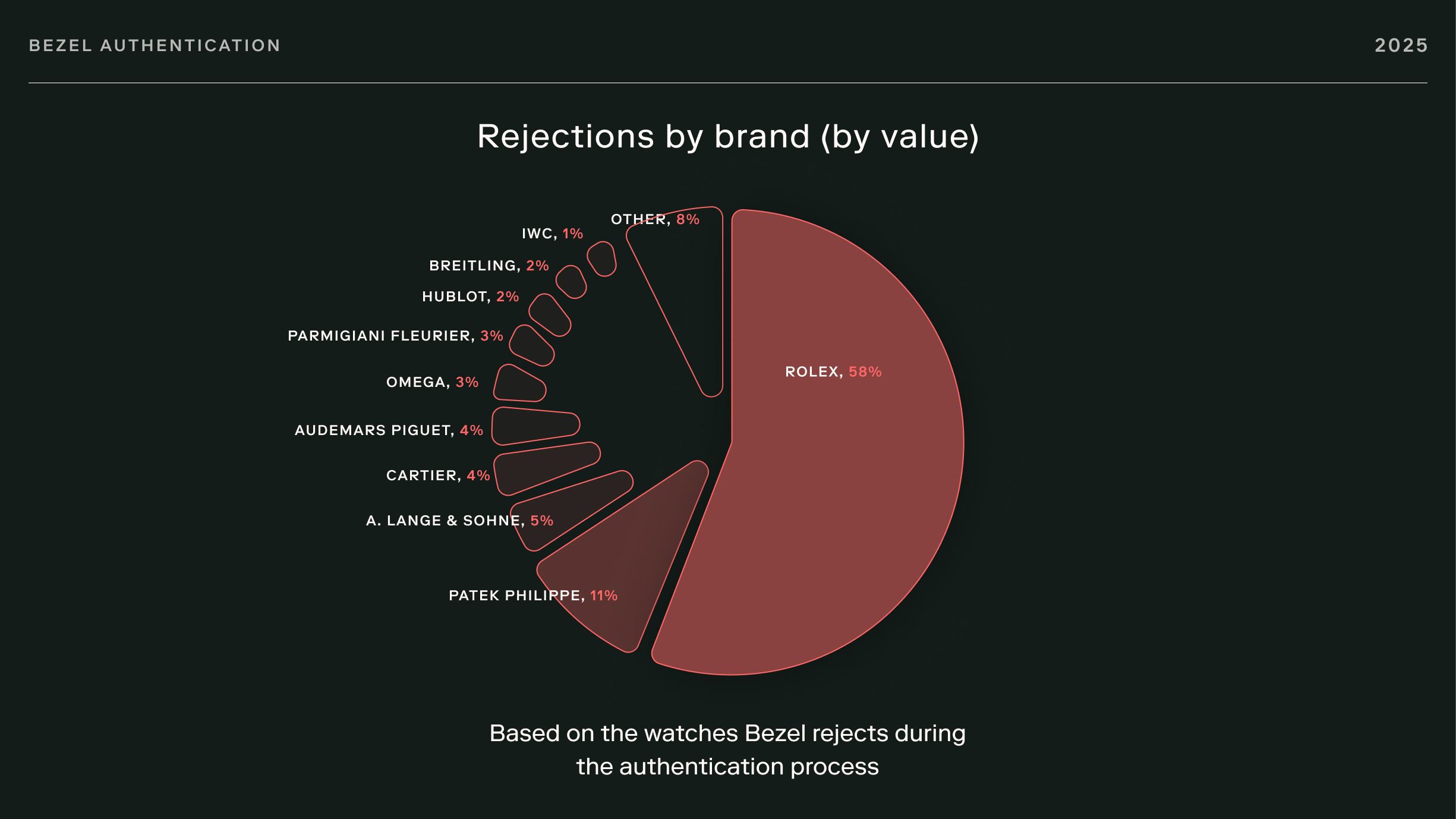

The values of rejected watches in 2025 show how broad the risk really is. The average value of a rejected watch reached $10,679. Authentication failures were not confined to low-end or fringe listings. At the same time, rejected watches spanned a wide range of price points, from a minimum of $950 to a maximum of $147,000. The spread makes one thing clear: price is not protection, and risk does not disappear simply because a transaction is smaller.

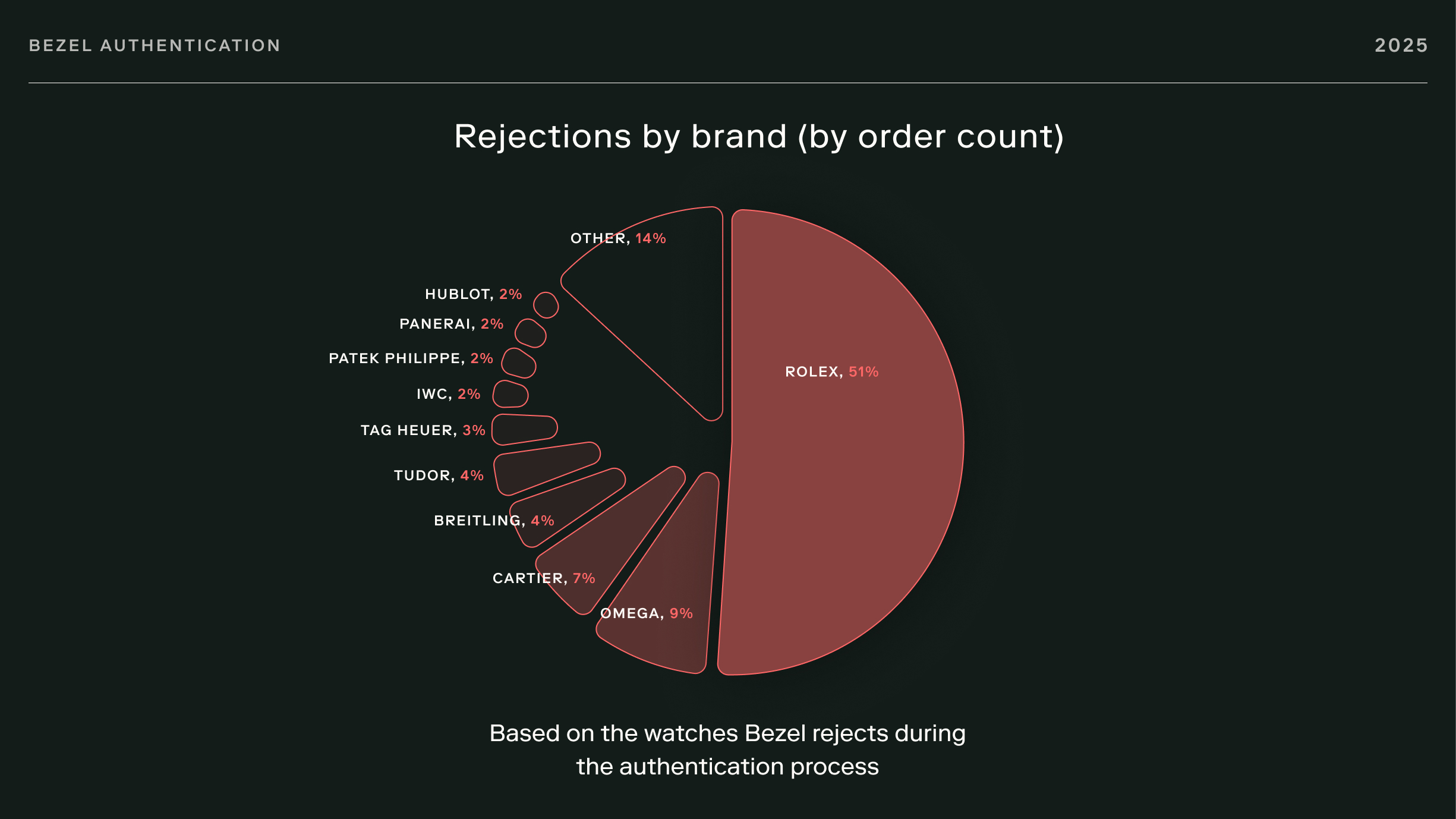

When viewed by brand, rejection patterns in FY 2025 closely tracked those seen earlier in the year, reflecting both consistent collector demand and the incentives that follow it. Rolex accounted for 51% of all rejected watches by count, consistent with its outsized presence across the secondary market. Omega followed at 9%, with Cartier at 7%, and the remaining top brands each at 2%-4%.

These percentages are not interchangeable. A rejected Patek Philippe, A. Lange & Söhne, or similar ultra-luxury listing can carry a very different downside, where one compromised example can turn into a six-figure mistake. Watches outside the top ten brands still made up 14% of total rejections, reinforcing that authentication challenges extend well beyond any single manufacturer or segment.

As in prior years, the reasons for rejection covered a wide range of issues, from non-period-correct components and undisclosed alterations to discrepancies in condition and functional shortcomings identified during in-house inspection. Taken as a whole, FY 2025 rejection data reflects a market under strain, and a verification process designed to absorb that strain without compromise.

The following cases show how these risks surface in practice. Each captures a different kind of breakdown we saw in 2025, from counterfeit documentation to internal modification and component-level fraud. In every instance, these issues were identified during our in-house authentication process, stopping compromised pieces from reaching buyers and from re-entering the market later with the same problems intact. Each case appears here in condensed form. More detailed examinations and additional reporting from Bezel’s in-house authentication team can be found in the Bezel Journal.

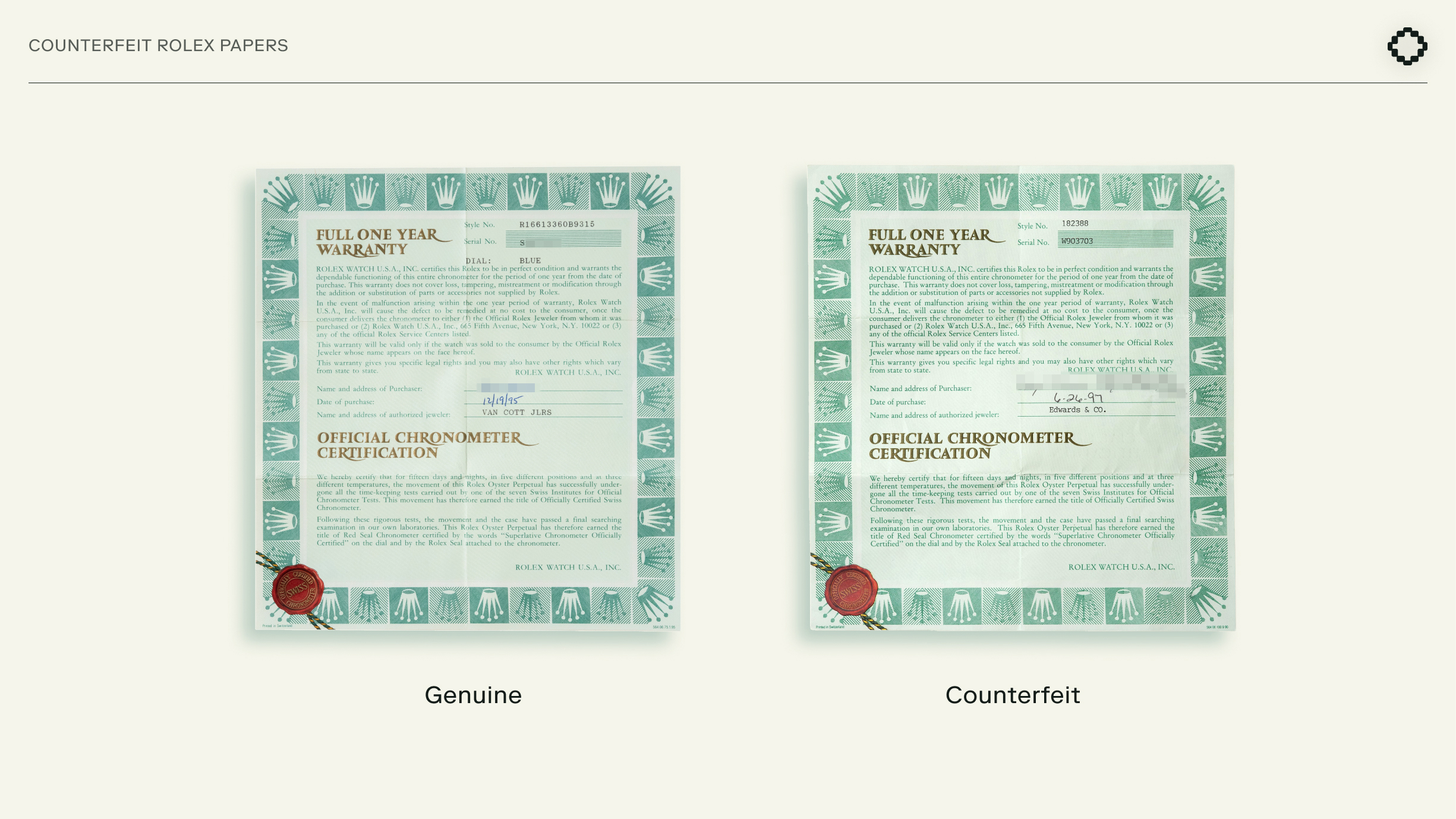

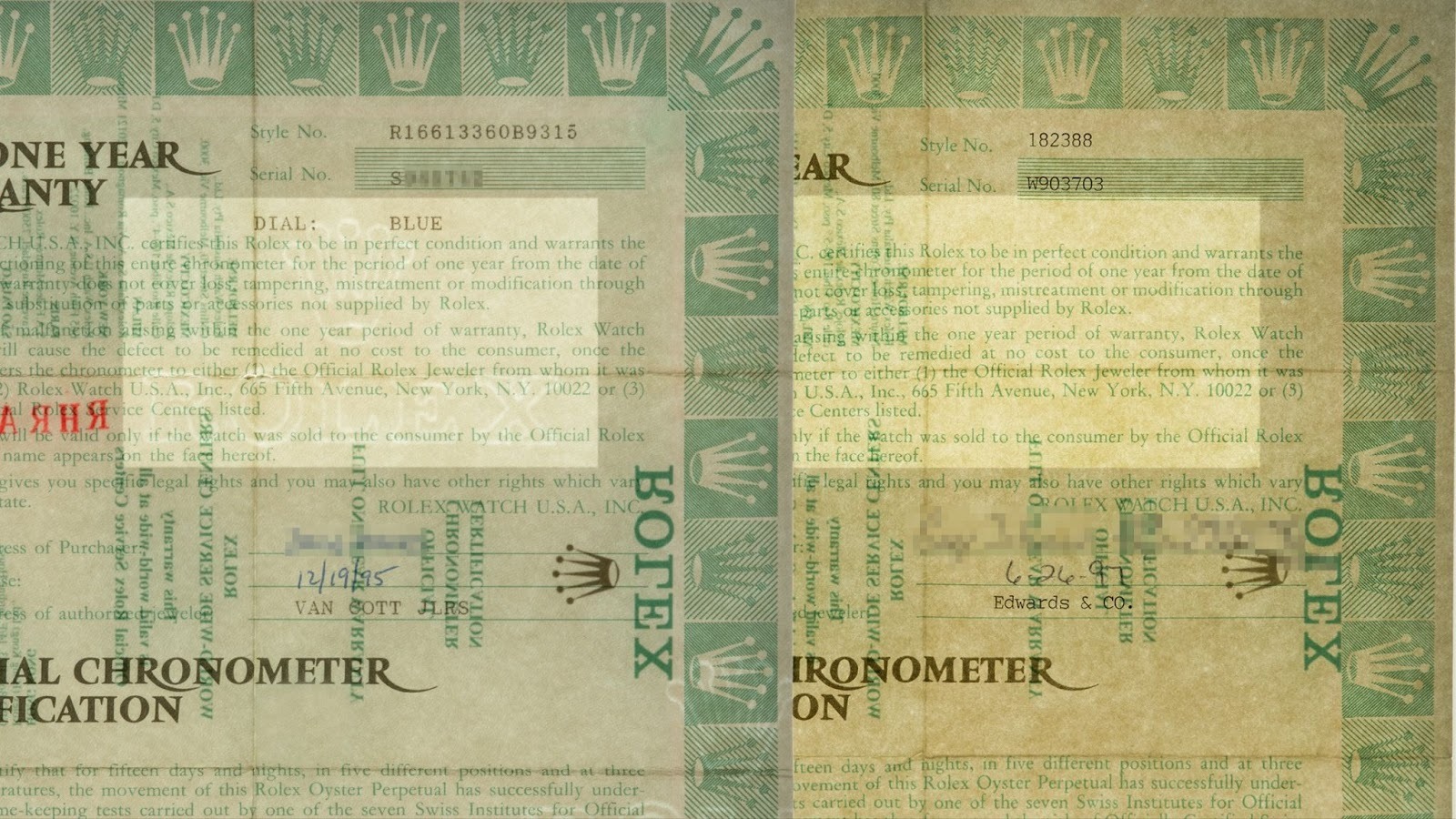

A yellow gold Rolex Day-Date 36 was submitted to Bezel as a purported full set from the mid-1990s. Once the watch, box, and accompanying papers reached Bezel HQ, they moved through the standard in-house authentication workflow.

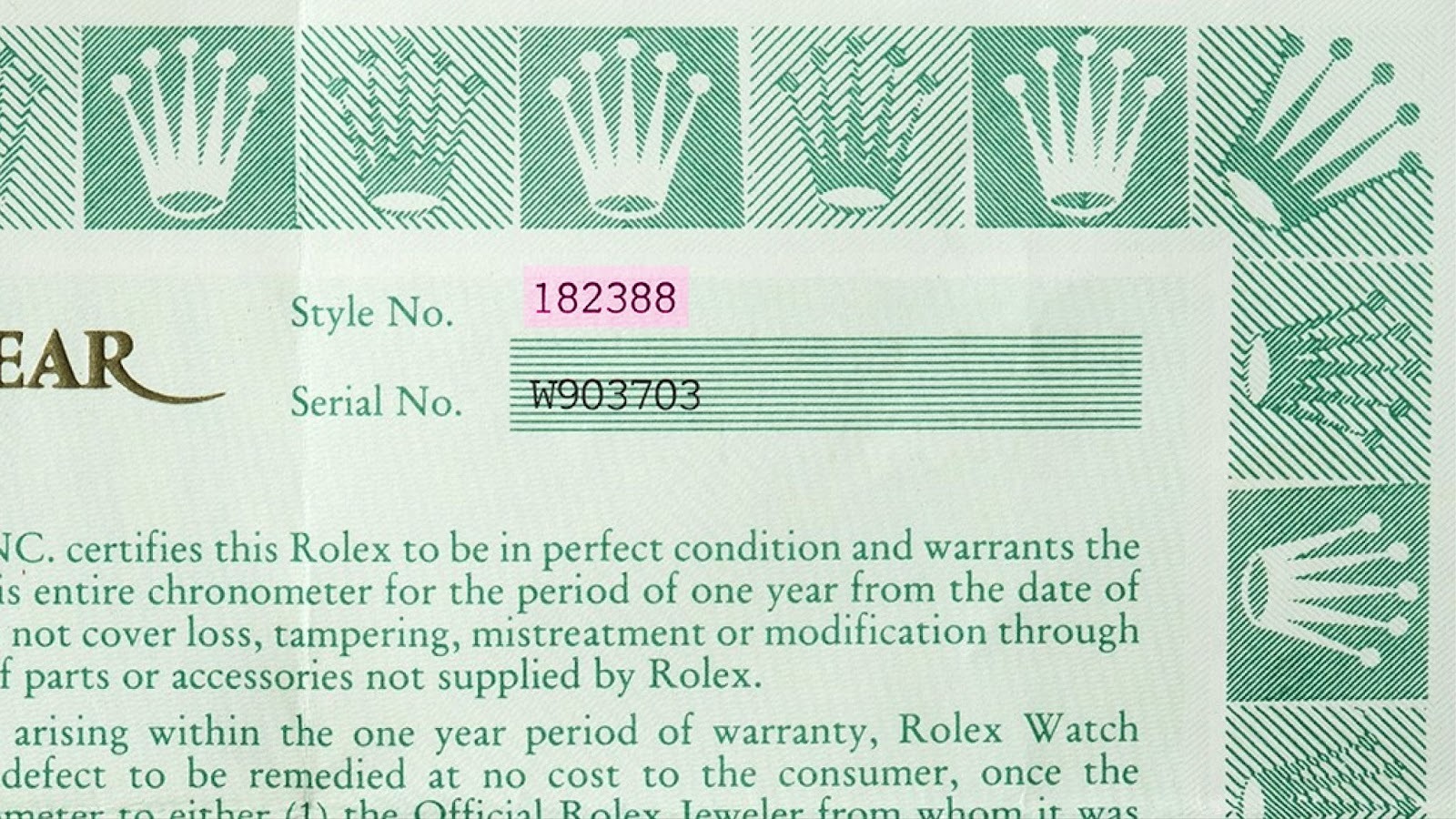

The watch itself checked out and matched the listing. The guarantee papers were next. They listed a W serial number, placing production around 1994–1995. Authentic paperwork from this period follows a specific printing format and includes faint coronet and text watermarks that become visible when backlit. When backlit, the watermarks never appeared.

Further comparison revealed additional inconsistencies. The gold foil text used for the warranty and chronometer certification differed in tone and finish from verified examples from the same era. More notably, the reference number printed on the document was “182388,” which does not correspond to any valid Rolex Day-Date reference. A correct yellow gold Day-Date from this period would have been marked “18238.”

Individually, each detail might have raised questions. Taken together, they confirmed the papers were not authentic.

Because the watch was paired with counterfeit documentation, the set was deemed misrepresented. The buyer was notified, the transaction was canceled, and Bezel’s concierge team assisted in sourcing a verified full-set replacement.

As Ryan Chong, Bezel’s Chief Marketplace Officer, notes, “There’s a lot of scholarship related to the authentication of watches. There’s not much out there when it comes to accessories, and that’s where the experience of our team is crucial to authenticating boxes and papers.”

Although the watch itself was genuine, the counterfeit papers materially altered its perceived value and provenance. The case illustrates how misrepresentation increasingly occurs not through the watch but through the elements that shape how a watch is valued. For a deeper examination of this case and counterfeit documentation as a whole, read the full story in the Bezel Journal.

The attempted sale of a Cartier Tank Must XL, reference WSTA0053, offered a clear example of how convincing modern counterfeits can appear when viewed only at the surface. Following the purchase, the watch was sent to Bezel for standard post-transaction authentication.

At first glance, it held together. The silhouette aligned with expectations. Familiar proportions. Nothing immediately suggested concern. Under closer review, that confidence began to erode.

Under magnification, the dial began to give itself away. The surface finish fell short of what you’d expect, and the typeface lacked the consistency seen on verified Cartier examples. The numerals, too, were subtly off in shape. The case and bracelet reinforced the doubt, with engravings and finishing outside Cartier’s usual execution. With several inconsistencies now apparent, the watch was escalated to Bezel’s in-house watchmaking team.

Inside the case, the movement proved decisive. Instead of Cartier’s Caliber 1847 MC, the watch contained a Miyota movement that had been cosmetically altered to resemble a Cartier caliber at a glance. While reliable in its own right, Miyota movements are not used by Cartier in this model.

The watch also included an authentic Cartier guarantee card that did not correspond to the piece in any legitimate way. Rather than documenting provenance, it appeared intended to reinforce credibility.

The watch was rejected, the sale was canceled, and the buyer was refunded. As Ryan Chong explains, “When someone buys a watch like this, they’re not looking for something close. They’re expecting exactly what’s represented.”

This case reflects the increasing sophistication of modern counterfeits, which often aim not for perfection, but for coherence. Without disassembly and movement-level inspection, watches like this can easily pass casual review. The full dissection of this counterfeit and how it was identified is documented in the Bezel Journal.

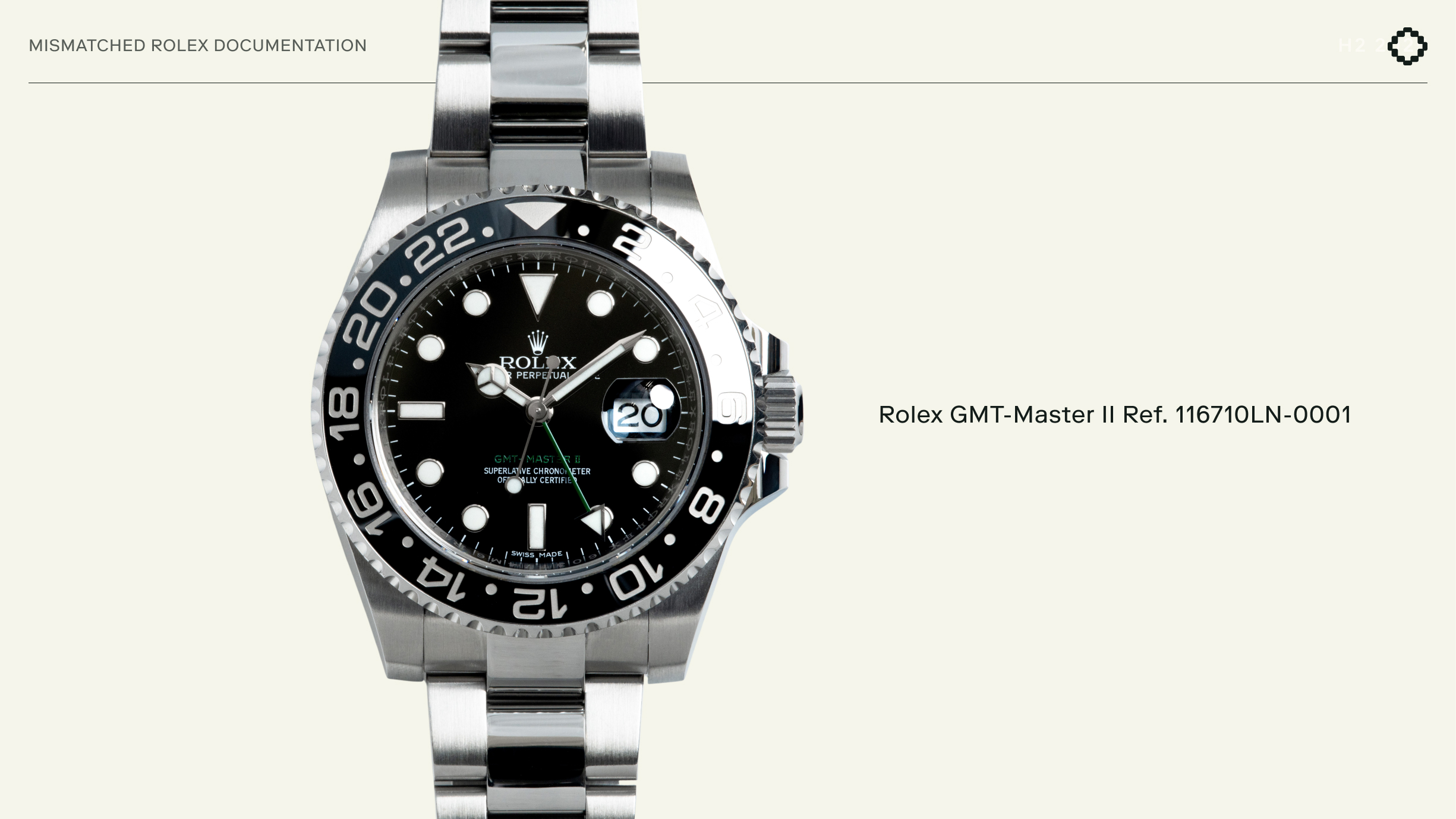

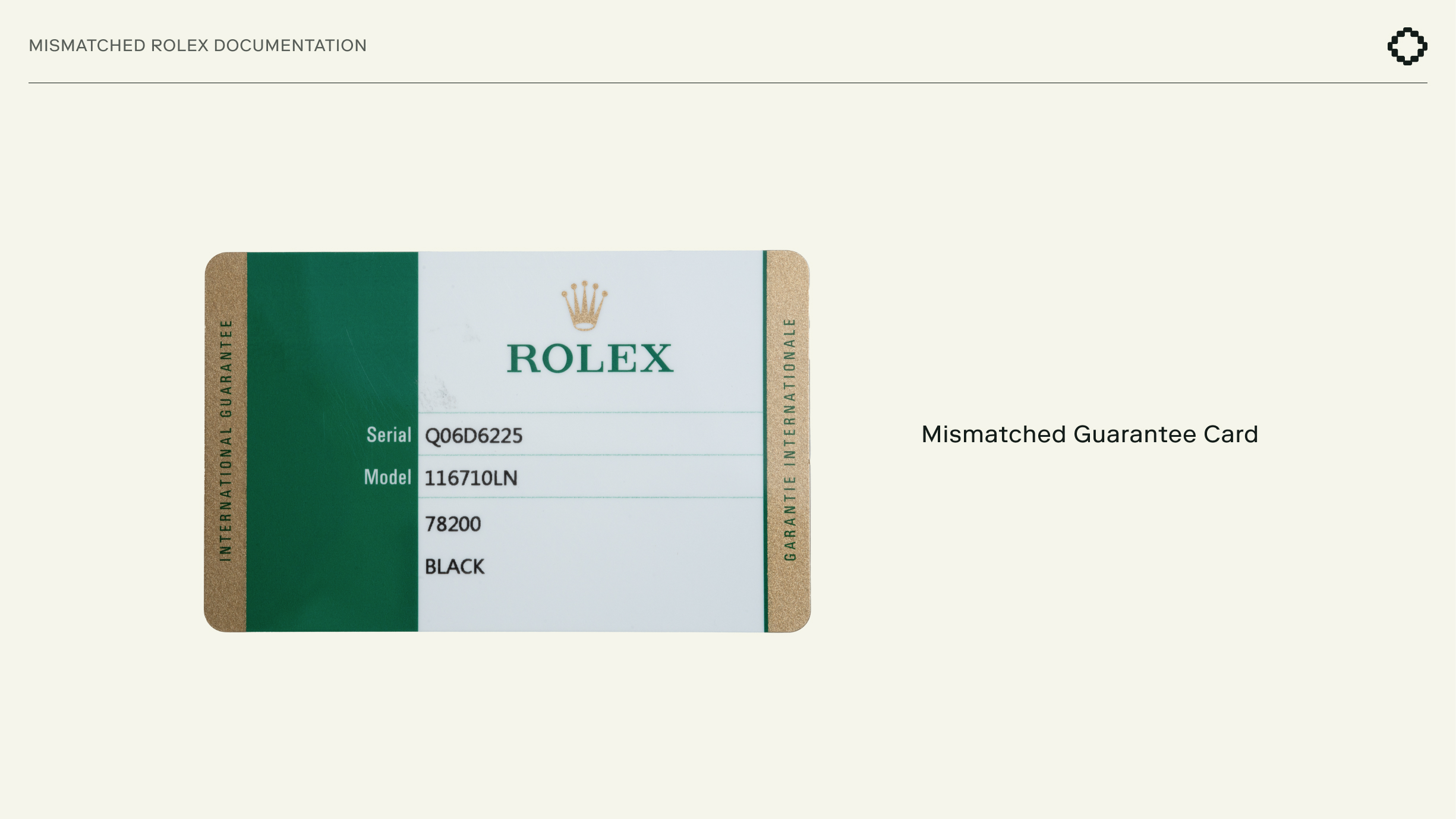

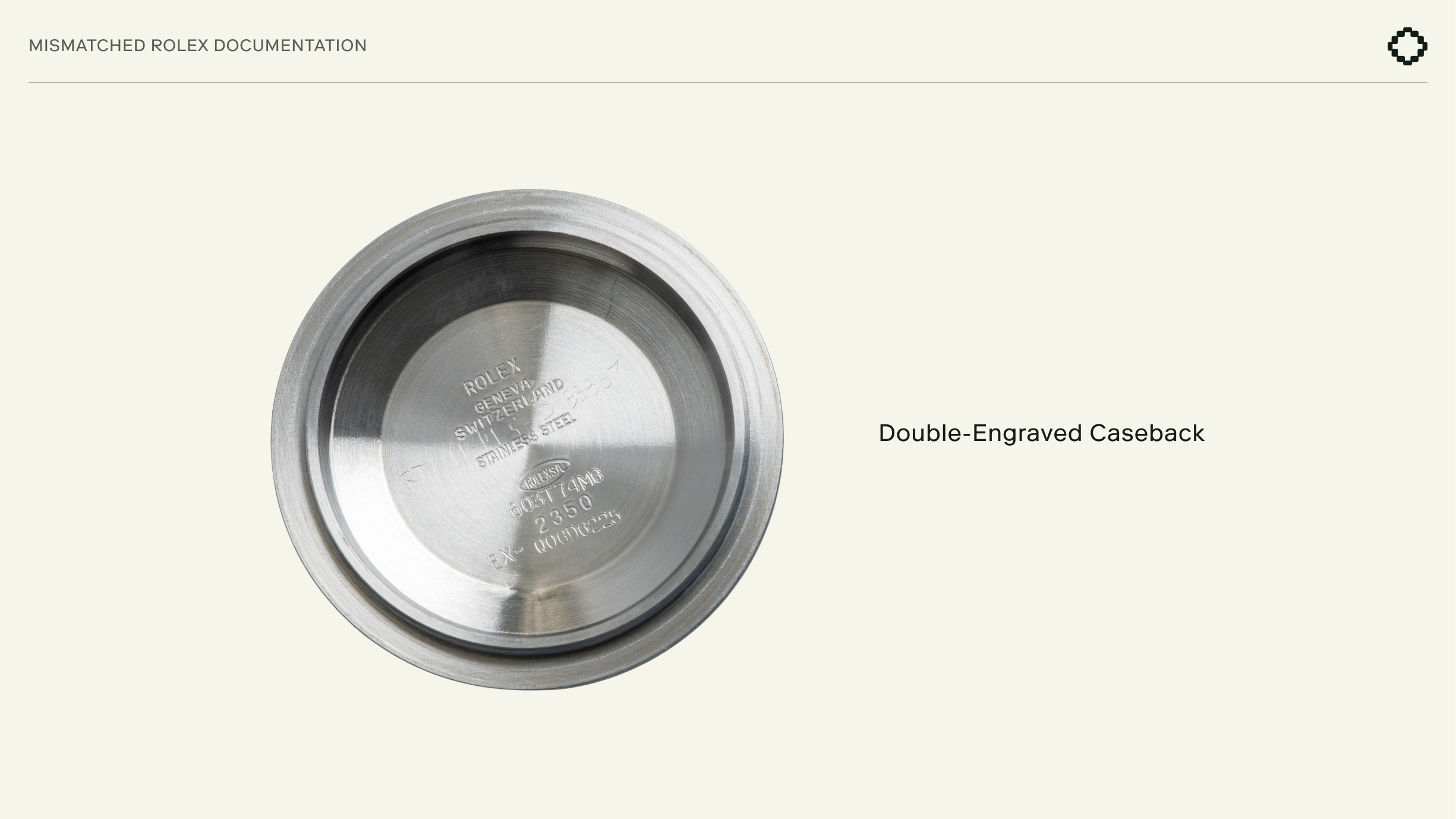

A stainless steel Rolex GMT-Master II Ref. 116710LN-0001 was submitted to Bezel, along with its accompanying warranty card, as part of a recent transaction. At first pass, it looked correctly represented. The condition matched the seller’s description, and the external markings were in line with what you’d expect.

Authenticators began where they always do, by verifying the watch’s identifying numbers. The serial on the rehaut matched the serial between the lugs, confirming internal consistency within the case.

The first break in that consistency appeared when those serials were compared with the warranty card. Although the card itself was authentic, the serial number printed on it belonged to a different watch. The watch was then routed to Bezel’s in-house watchmaking team for deeper inspection.

Rolex already repeats serial information in multiple locations. The extra engraving inside the caseback served no functional purpose. During movement inspection, watchmakers discovered it. Rolex engravings follow strict standards for placement and execution, and this marking did not conform to factory production standards. It appeared intended to visually link the watch to the mismatched warranty card. As a result, the watch would be refused by Rolex for service and would be difficult to represent cleanly on the secondary market.

The transaction was canceled, and Bezel’s concierge team assisted in sourcing a correct example.

As Ryan Chong explains, “Buyers tend to focus on whether a watch is real. What’s less obvious is whether it remains serviceable and defensible long term. That’s where deeper inspection becomes critical.”

This case illustrates how authenticity is not always binary. Even genuine watches can carry modifications that materially affect future ownership, service, and resale. The complete investigation into this instance and its long-term consequences appears here in the Bezel Journal.

An 18k white gold Audemars Piguet Code 11.59 Chronograph arrived at Bezel following purchase for authentication. From the outside, it matched the listing. The case showed no visible wear, the dial was clean, and the overall presentation suggested a carefully kept example.

At first pass, nothing stood out. Closer handling changed that assessment.

When the watch was turned over and examined through its sapphire caseback, authenticators noticed visible scuffing on the rotor of the Caliber 4401 movement. The wear was pronounced and inconsistent with normal operation. Its pattern suggested prior removal or internal handling rather than incidental contact.

Further inspection confirmed it. The marks looked unlike what is to be expected of factory handling and didn’t resemble professional service, either. It read like undisclosed internal work on a watch still represented as clean and under warranty.

The watch itself was genuine, but it no longer met Bezel’s condition standards or what the buyer had agreed to purchase. Internal mishandling can affect service eligibility and long-term reliability, which is why the transaction stopped there. The buyer was notified and refunded, and Bezel’s concierge team assisted in sourcing a correct example.

This case highlights a less visible category of risk in modern collecting. A watch can look pristine on the outside while carrying internal history that materially affects value, serviceability, and future ownership. The full inspection record and analysis of this case can be found in the Bezel Journal.

As a marketplace, Bezel’s objective remains straightforward: to keep inventory aligned with what collectors are actually seeking. In FY 2025, activity across what clients bought, what they followed, and what they already owned moved largely in parallel. Purchases reflect transactions completed on Bezel. Wants capture the references users choose to track, along with the alerts they receive as listings appear or prices move. Owned watches are those clients register inside their Bezel collections, a layer that also supports collection tracking and insurance coverage.

Stepping back, the overall shape of that activity looked much like FY 2024. Preferences held steady even as conditions tightened and pricing adjusted, suggesting that underlying collector behavior changed far less than the market environment around it.

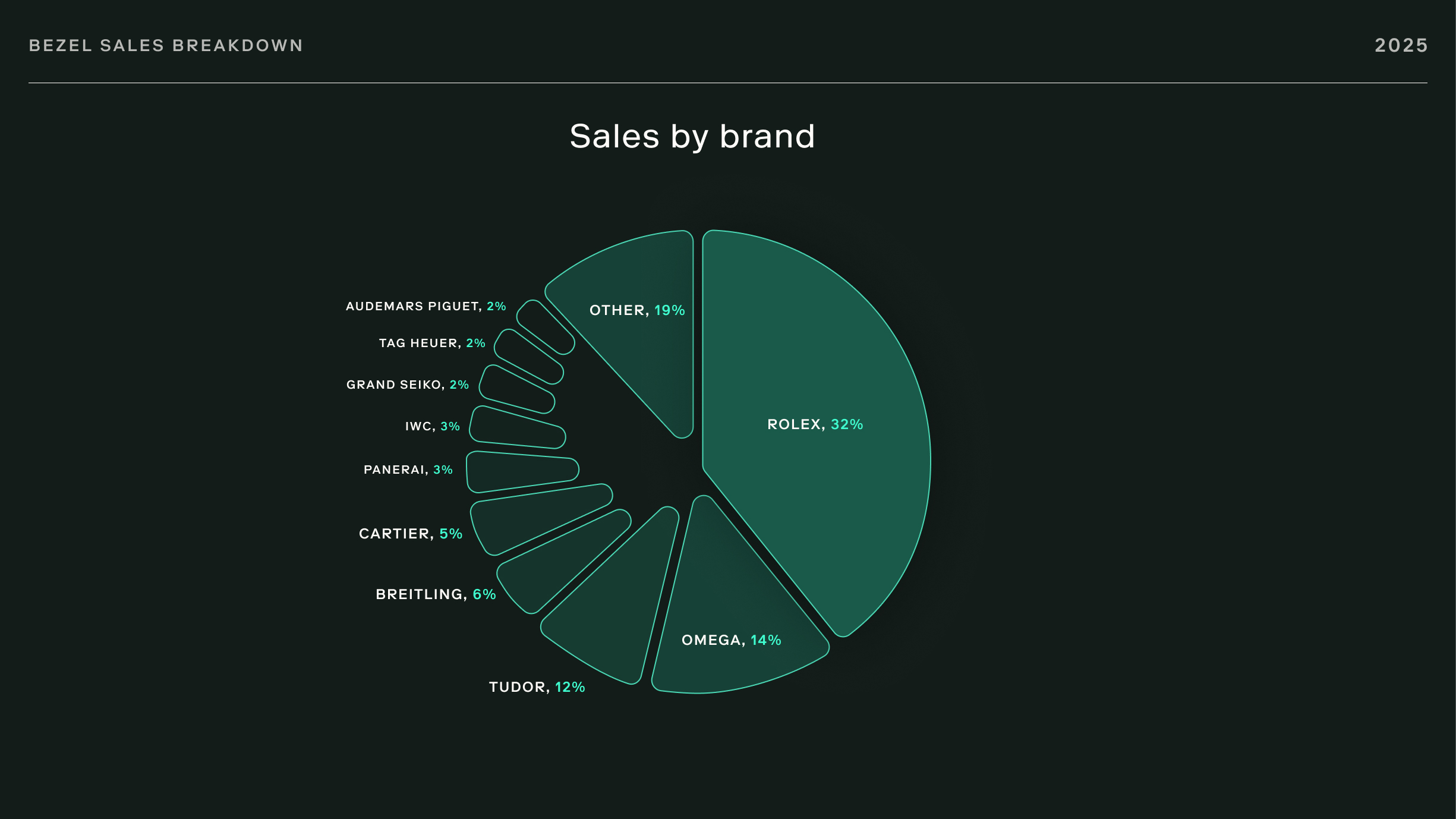

By brand, the leaders stayed familiar. Rolex continued to lead by a wide margin, as it did in FY 2024. The most visible change came on the purchase side, where Tudor gained share and continued closing the gap with Omega. Breitling and Cartier followed at mid-single-digit percentages.

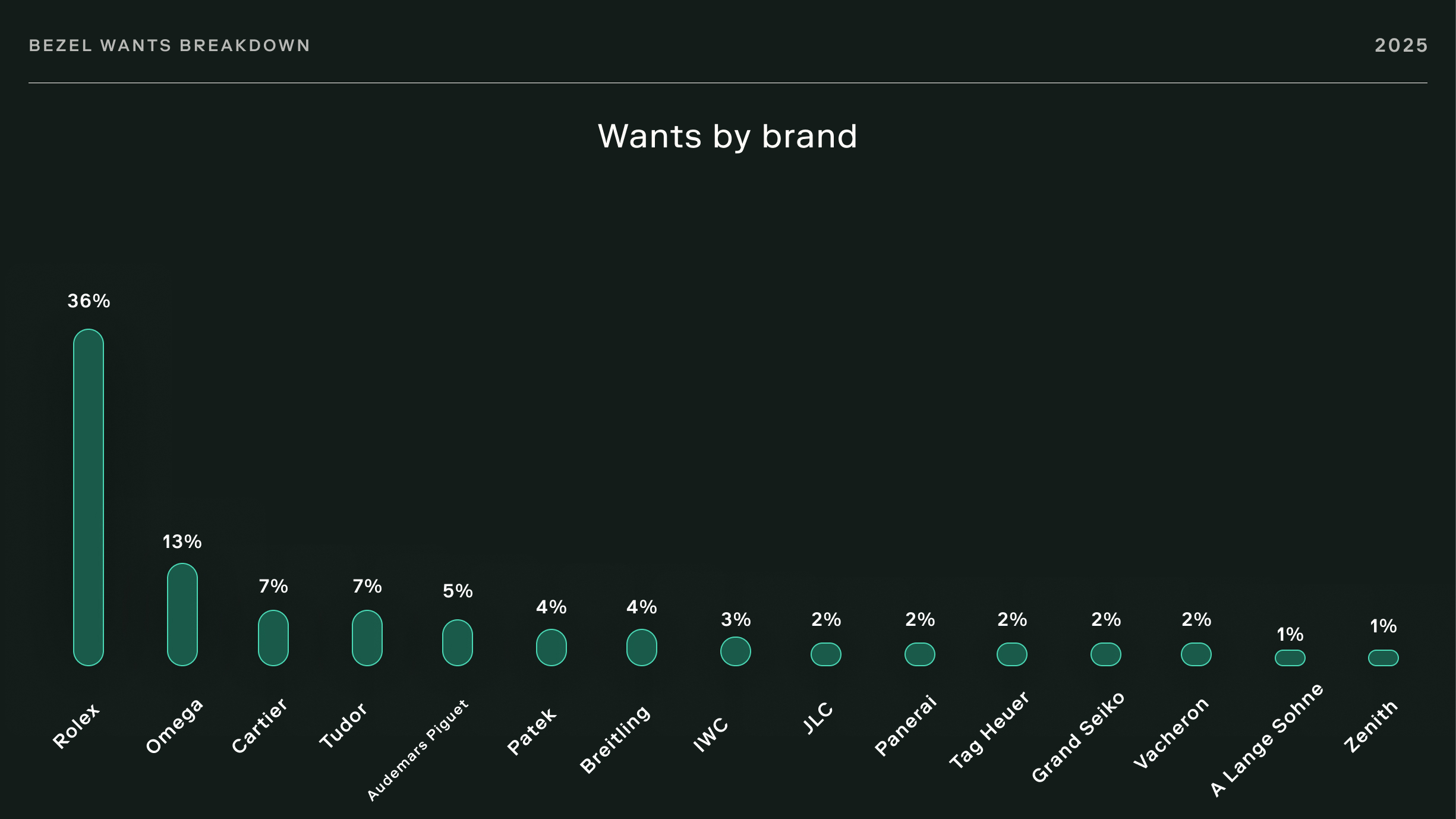

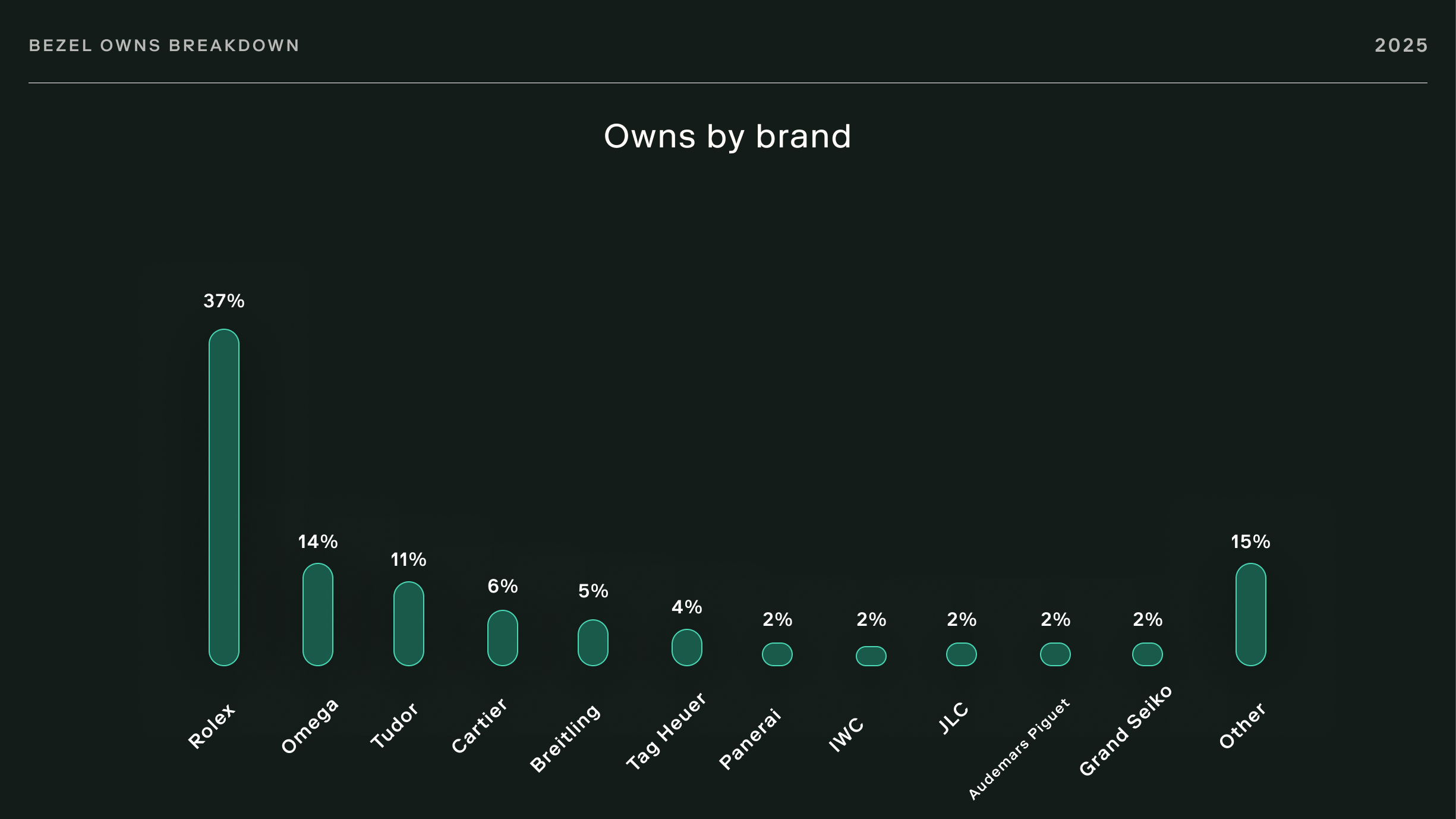

Want activity tracked closely with this distribution. Ownership data followed a similar pattern. Acquisition, aspiration, and long-term retention still moved together on the platform.

More subtle divergence appeared outside the top tier. Parmigiani Fleurier and a growing set of independents showed up more often in completed transactions than in expressed Wants. In many cases, they sold before ever building meaningful Want activity, and they often traded below retail. The throughline is straightforward: buyers are making room for finishing and watchmaking that can out-punch the name on the dial, especially while supply remains constrained.

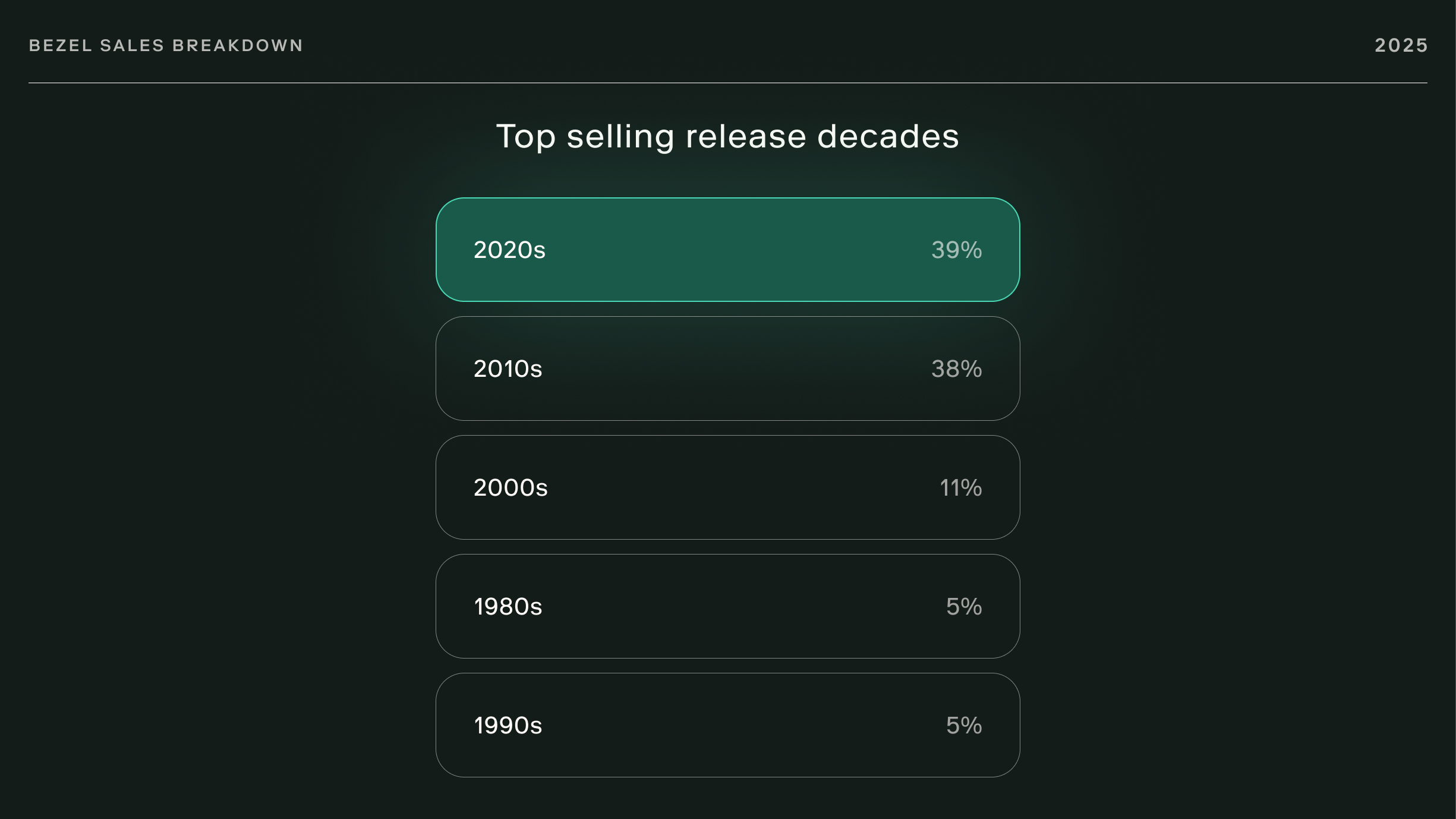

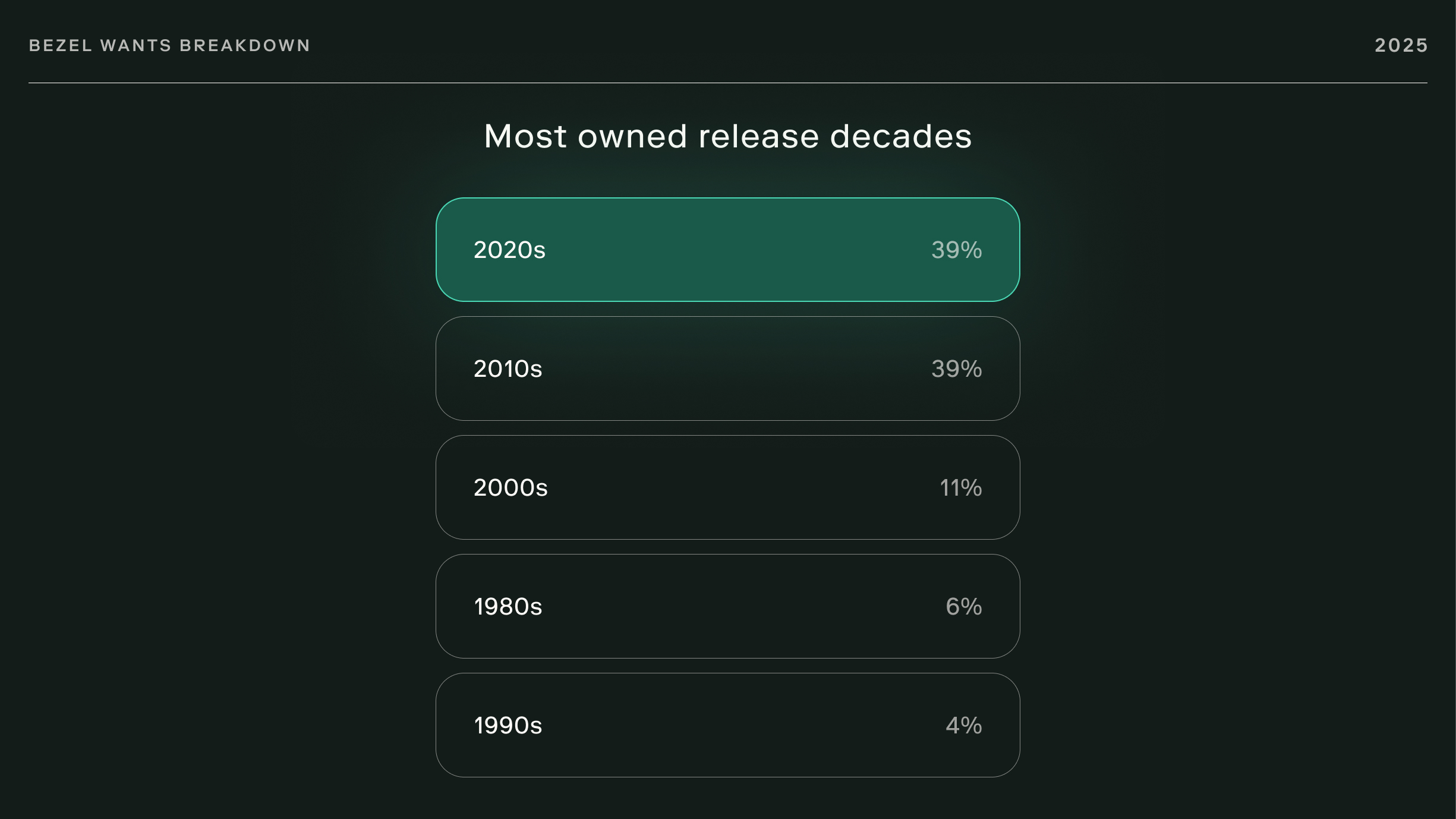

By release decade, activity stayed overwhelmingly modern. That mix was effectively unchanged from FY 2024, when those same two decades already represented more than three quarters of Wants and purchases. Watches from the 2010s and 2020s accounted for nearly 80% of orders, Wants, and Owned watches. Earlier decades still held their share, even as modern releases dominated volume.

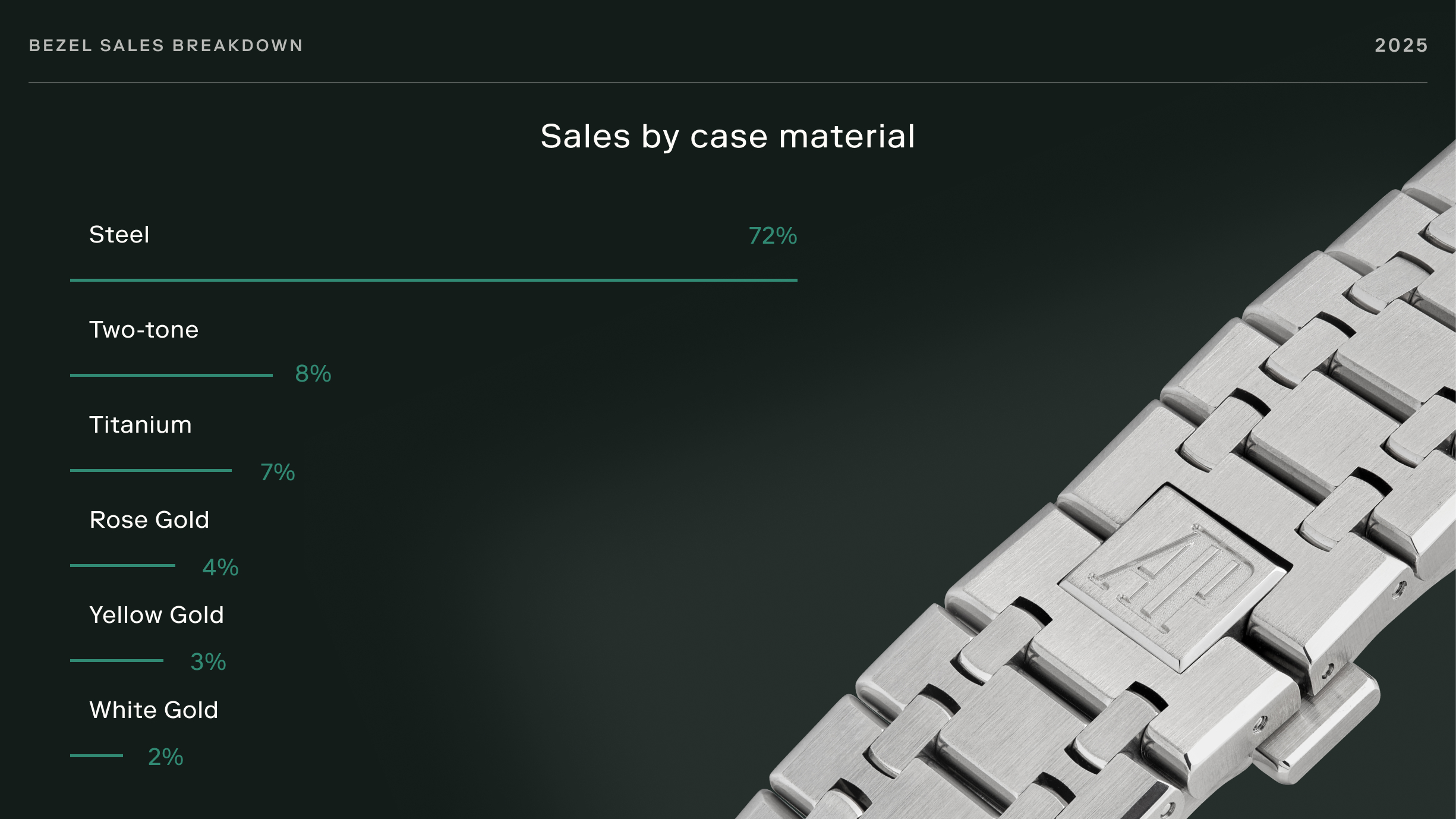

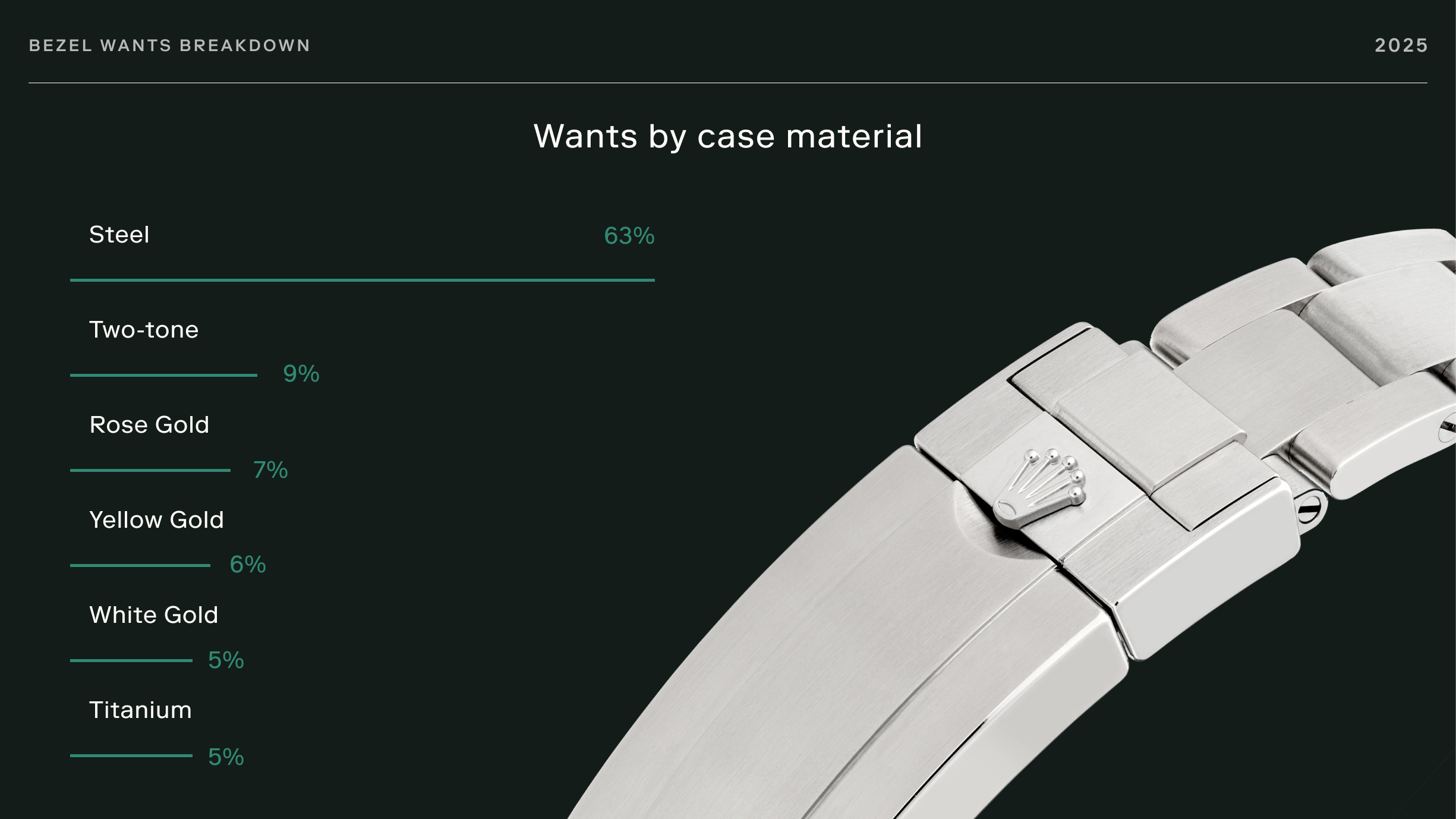

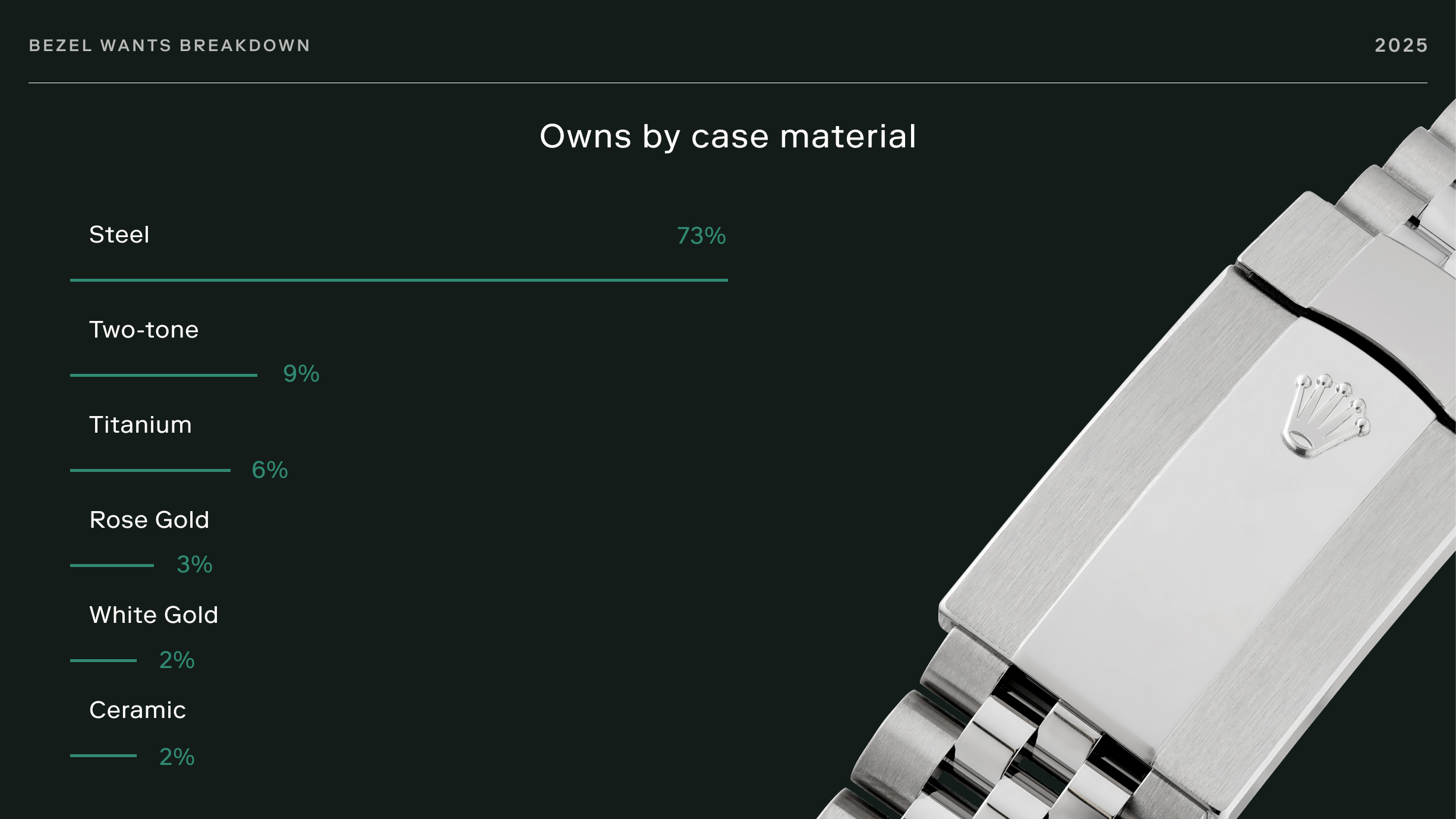

Case material stayed steady, with preferences barely moving year over year. The mix looked much like FY 2024, when steel already dominated both purchases and want activity. That pattern held through 2025. Steel continued to account for the clear majority of wants, owns, and completed orders, while two-tone sat just under ten percent.

Titanium showed up slightly more often in actual purchases than in expressed wants, a small but telling signal that lighter, utilitarian watches are finding buyers even when they are not being actively chased. Precious metals remained a narrower slice of overall volume, but their share stayed broadly intact.

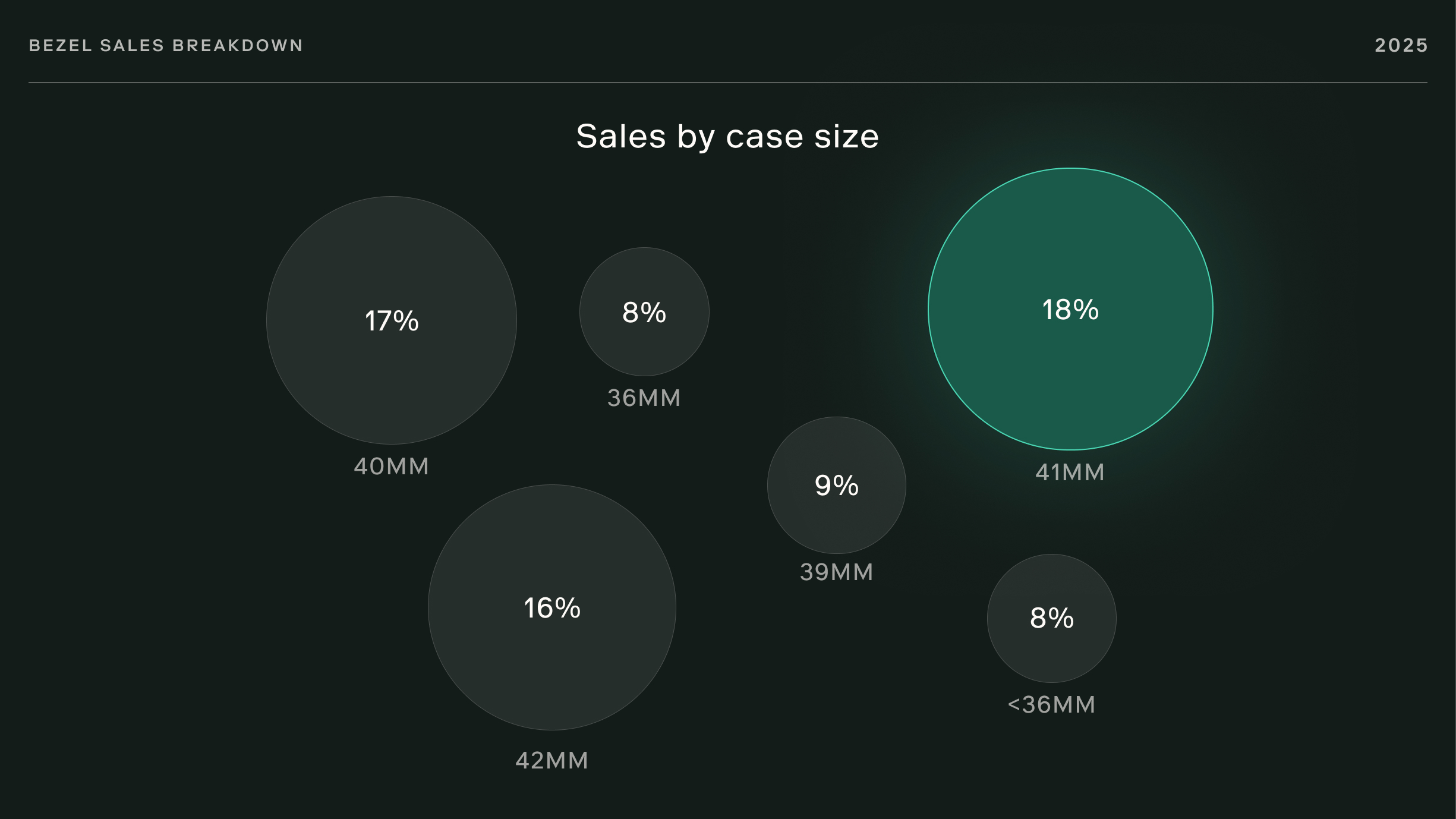

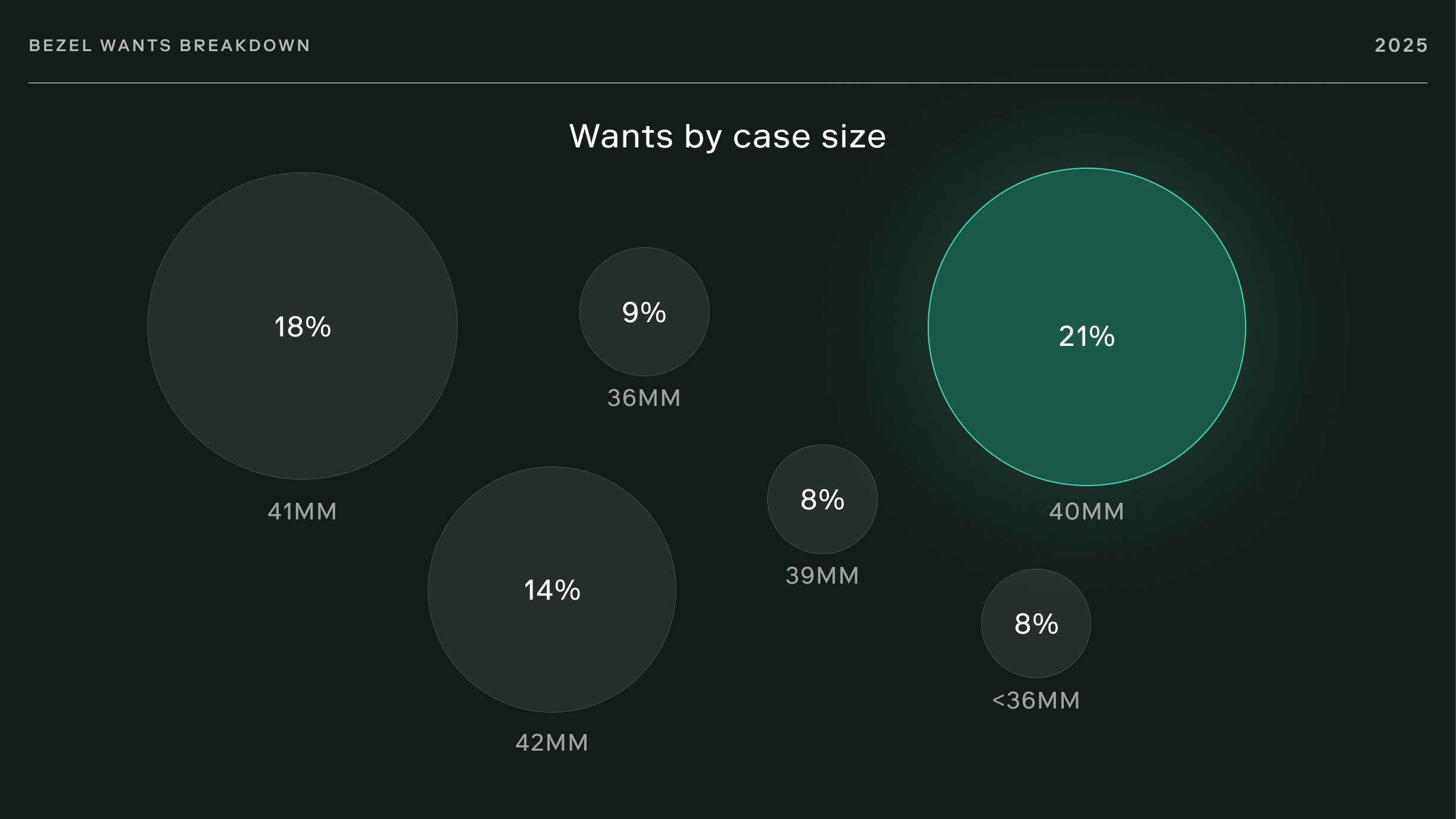

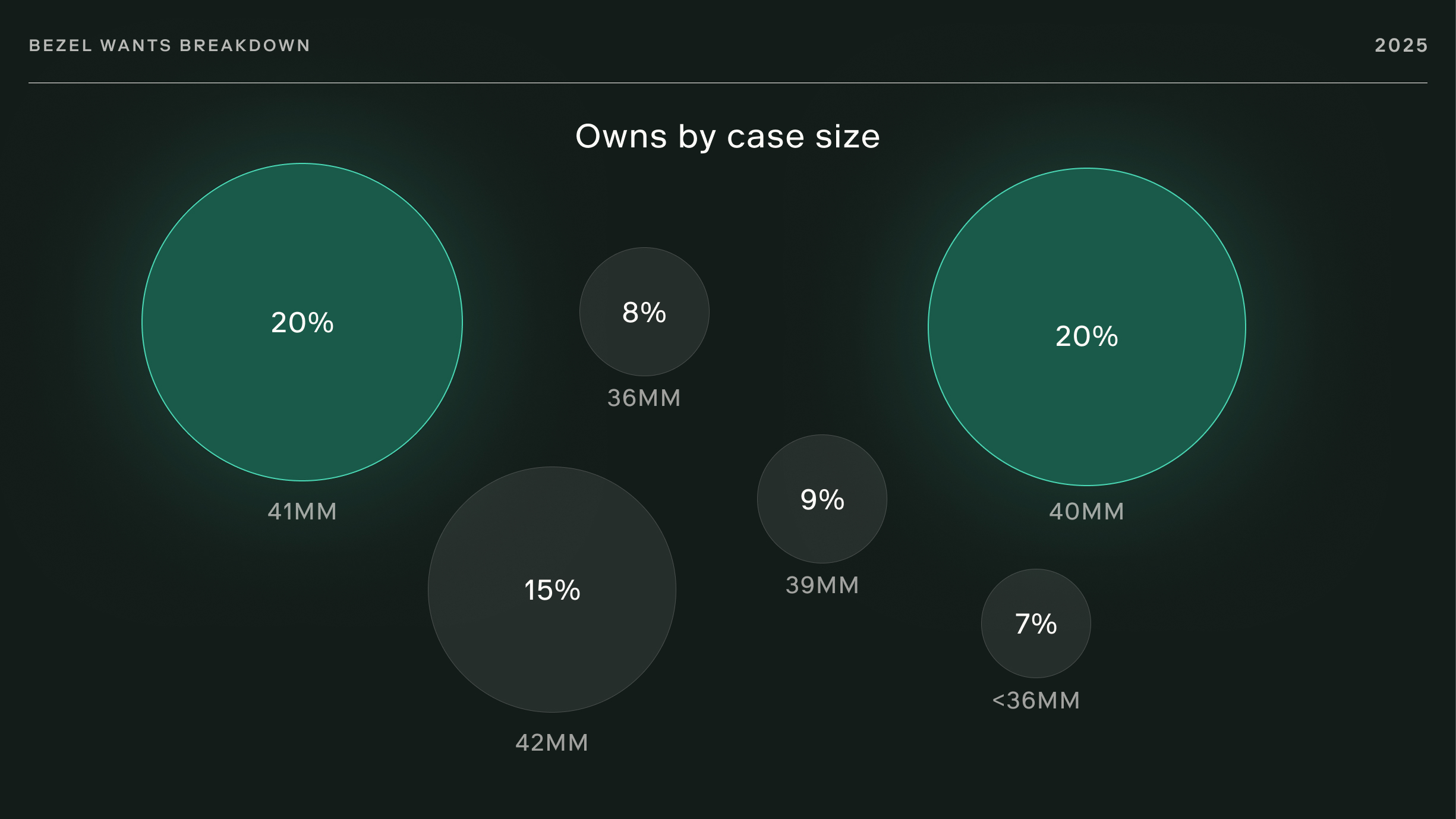

Case-size data showed a broad middle rather than a single dominant dimension. That center of gravity was unchanged from FY 2024, when 40 mm and 41 mm already represented the single largest combined size band across both wants and purchases. Cases above 42 mm still accounted for meaningful volume, and sub-36 mm stayed modest but consistent. 40 mm and 41 mm comprised the largest combined share, with adjacent sizes close behind. Non-circular cases stayed small and steady. More signature than swing.

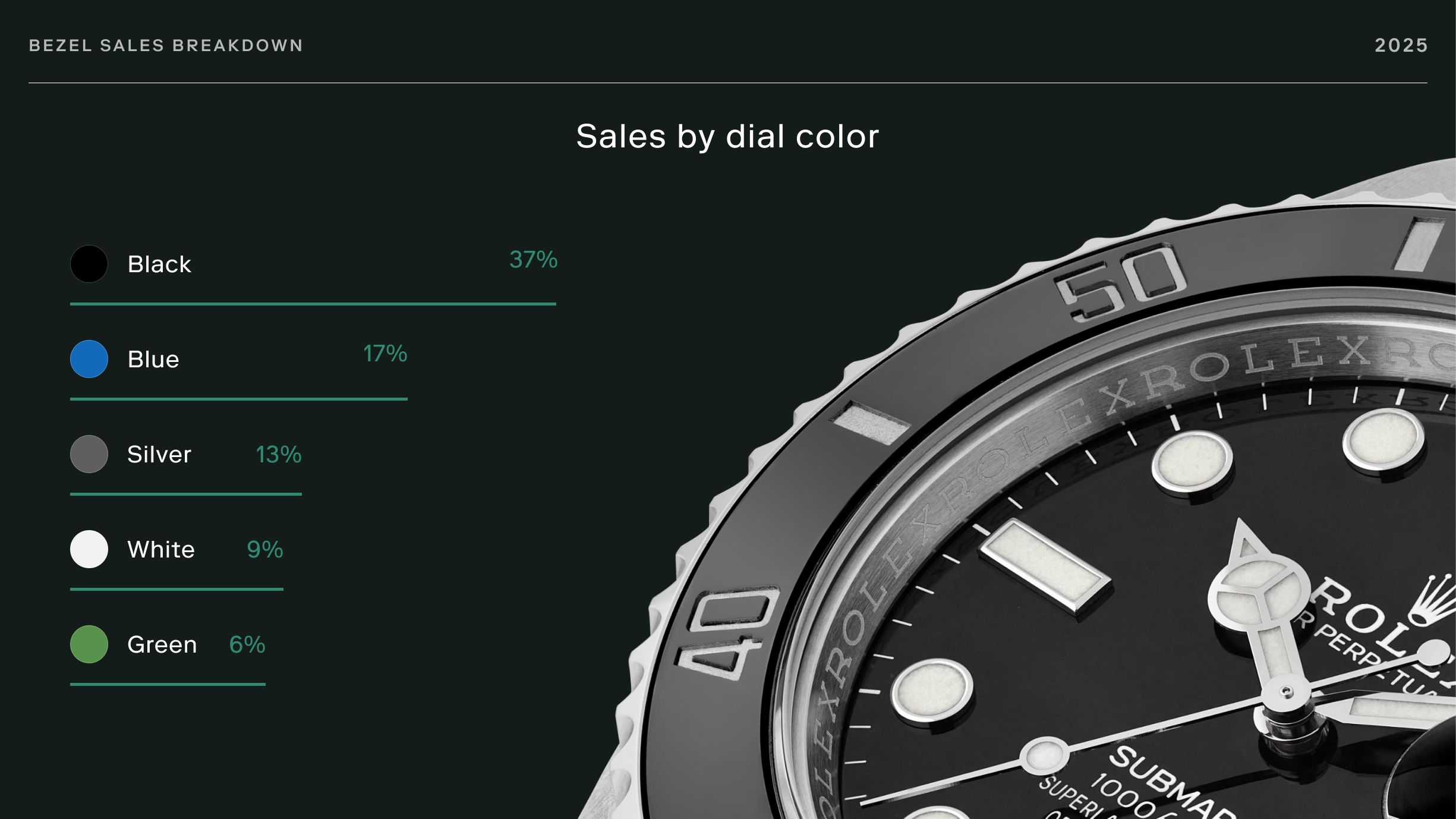

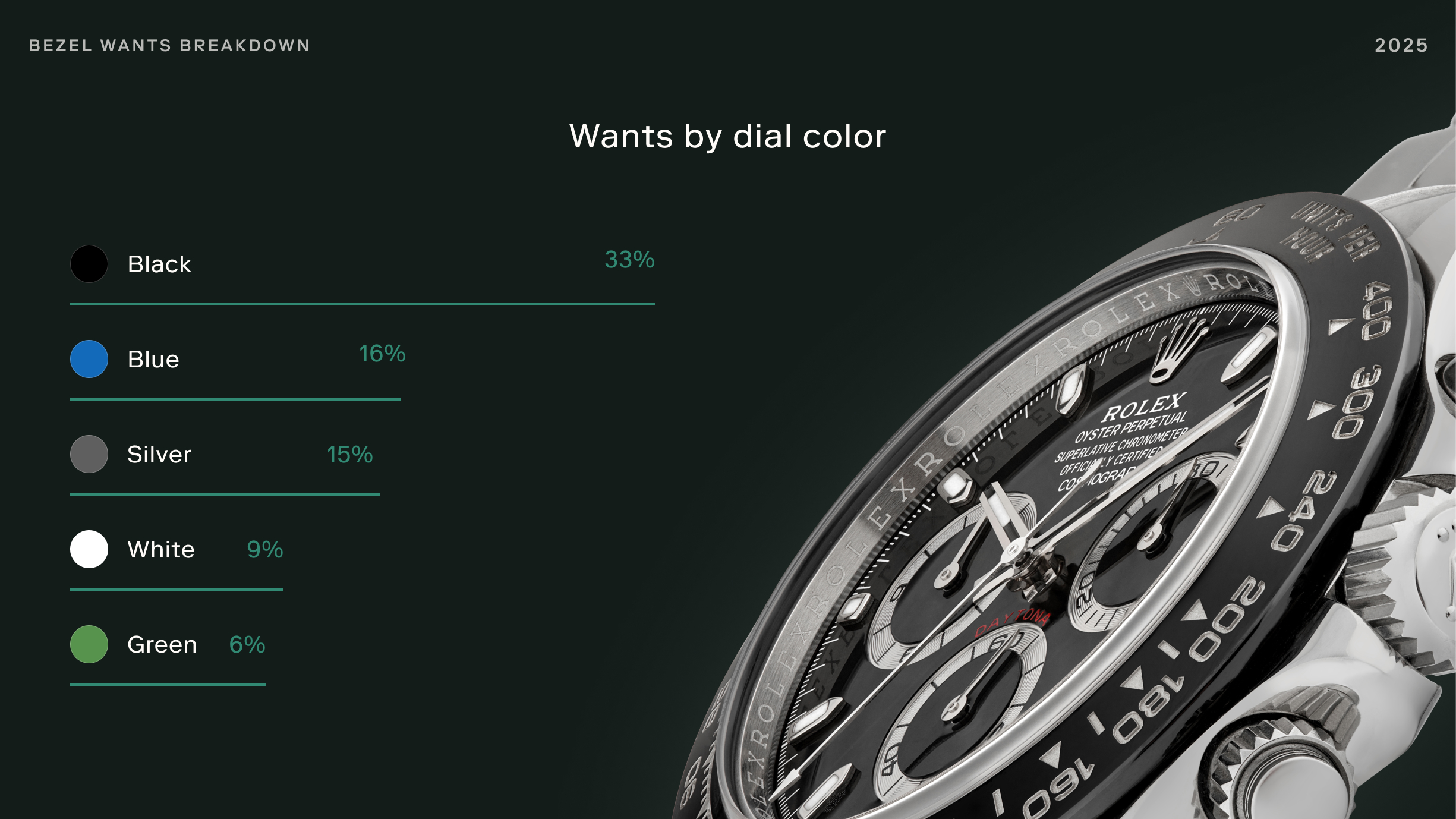

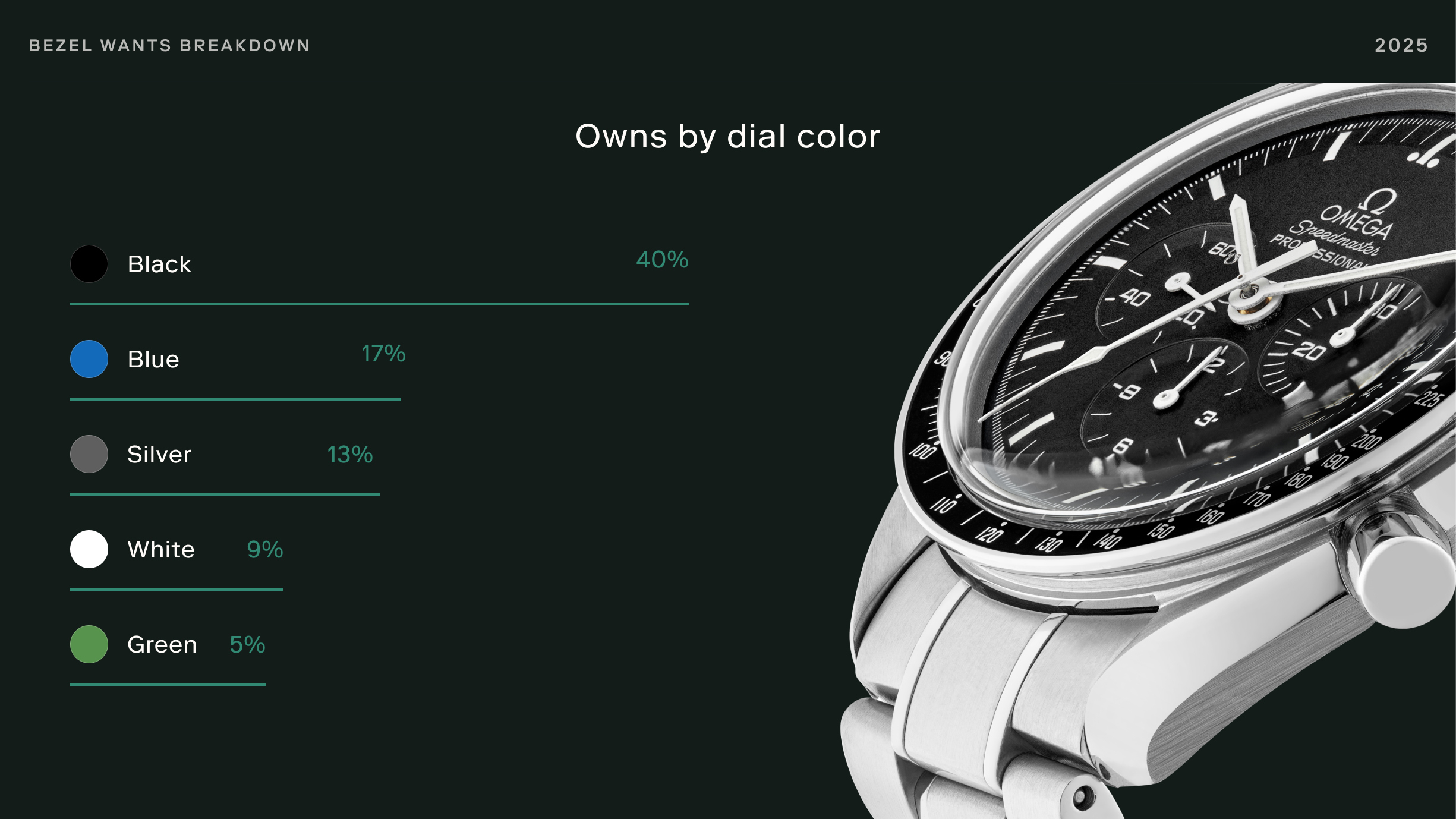

Dial color preferences stayed conservative. The ranking was effectively identical to FY 2024, when black, blue, and silver also dominated both want activity and completed sales. Black led 2025 across all measures, followed by blue and silver-toned executions. More expressive options remained in the low single digits. White held steady, with green, gray, and champagne in smaller but durable positions.

Taken together, FY 2025 looked less like a behavioral reset and more like a continuation of FY 2024 with slightly tighter supply, more selective buying, and a few subtle reallocations at the margin.

Across FY 2025, the watch market remained durable, but increasingly selective. Demand stayed present. Engagement followed. What shifted most meaningfully over the course of the year was not appetite, but availability, pricing structure, and how both buyers and sellers adapted to a more constrained environment.

Tariffs introduced the first layer of friction. In April, proposed duty increases sparked speculation and the acceleration of inventory movement as wholesalers and retailers fast-tracked imports ahead of potential cost increases. In August, Washington imposed a 39% tariff on Swiss imports, pushing landed costs significantly higher than in previous years. Pressure eased materially when a preliminary trade framework was agreed upon in November to cap tariffs at 15%, though elevated costs were sustained through the year’s second half.

Uncertainty persisted behind the scenes. Over the summer, executives from major Swiss manufacturers, including Rolex, engaged directly with U.S. policymakers, holding meetings both in Washington and during high-profile events such as the US Open Tennis Championships in New York.

Several Swiss brands raised retail pricing through H2, resetting replacement costs and narrowing the margin for discounting. In the secondary market, this created a clearer floor beneath certain segments, particularly for current production steel sports models and core references, where retail pricing once again shaped resale behavior.

Supply, more than demand, defined the year. Allocation remained tight. New inventory arrived selectively. Pre-owned availability reflected willingness to sell rather than buyer hesitation. On Bezel, transactions continued, but velocity diverged sharply across references and configurations.

Within that environment, pricing behavior separated more clearly. Modern steel icons stabilized. Core references in the Submariner, GMT-Master II, Royal Oak, and Nautilus families continued to clear within narrow bands. These models no longer behaved like speculative assets, but they retained their role as liquidity anchors, supported by scarcity, replacement cost, and persistent long-term demand.

At the same time, a number of previously inflated hype references softened materially, most visibly in stainless steel Rolex Daytona references, 15500-series Royal Oak references from Audemars Piguet, and core Patek Philippe Aquanaut configurations that had traded well above structural value during the post-pandemic surge. The correction was uneven, but consistent in direction. It looked more like normalization than waning interest. Mid-tier brands repriced more quietly. Values drifted lower through seller concessions rather than headline adjustments. The movement rarely drew attention. It still made the market more rational beneath the surface.

Independent watchmaking continued to gain interest, but liquidity bifurcated. A small group of recognizable makers and references cleared quickly and consistently. Others, despite technical merit, traded far less predictably. Craft and collectability proved insufficient on their own.

Sentiment remained measured. Buyers grew more selective. Sellers became more deliberate. Negotiation increased, but urgency did not. The market narrowed its focus rather than its participation.

By year-end, it had not expanded. It had not contracted either. It had settled. Tariffs altered cost, but not conviction. Pricing adjusted, but did not unravel. Supply constrained flow, but did not suppress demand. The result was a market increasingly shaped by fundamentals: scarcity, replacement cost, configuration, and long-term intent.

Gold added another source of pressure as the year progressed. Prices rose through 2025, pushing up costs across cases, bracelets, and dials, forcing adjustments across a broad set of precious metal references. Brands responded in kind by increasing retail prices. Replacement costs reset, not only because of tariffs, but because material economics left little room elsewhere.

In the secondary market, the effect was subtle but persistent. Gold models held their floors more consistently, with intrinsic value limiting downside and compressing the gap between retail and resale.

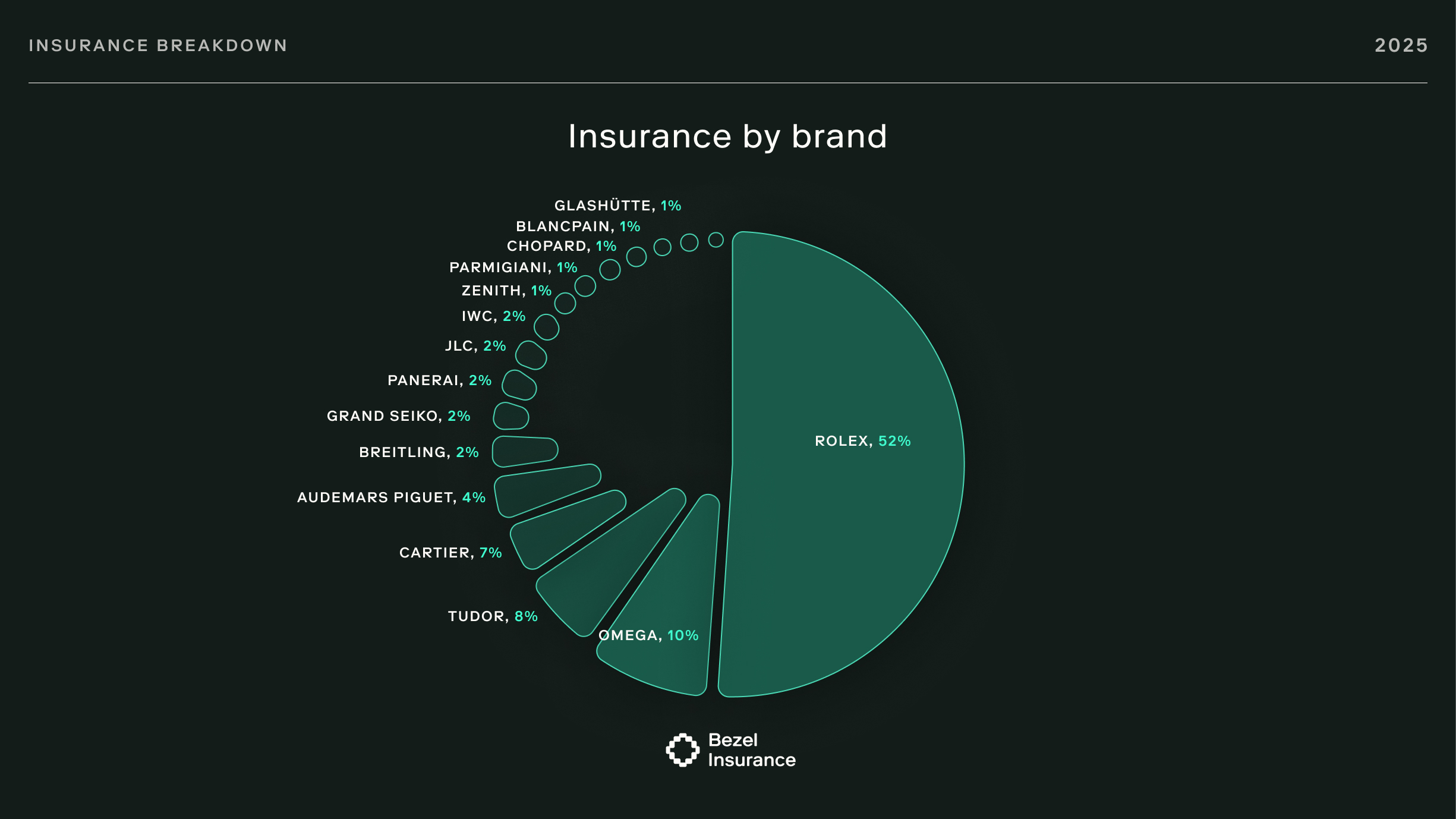

In the second half of 2025, Bezel introduced Bezel Insurance, a fully integrated watch insurance program underwritten by Chubb, a global leader in insurance and the leading personal lines insurer for high-net-worth families in the United States.

The decision to introduce insurance followed what we were already seeing on the platform. Watch values continued to rise, supply remained constrained, and collectors increasingly held meaningful value across multiple pieces rather than a single flagship watch. At the same time, traditional insurance options often proved fragmented or poorly suited to modern collecting—arranged after purchase, managed off-platform, and disconnected from the watches themselves.

Bezel Insurance was designed to close that gap. By pairing Bezel’s authentication-first marketplace with Chubb’s underwriting expertise, the program extends trust beyond the moment of purchase and into long-term ownership itself. Watches can be insured whether they were acquired on or off Bezel, with coverage structured around how collectors build, manage, and evolve their collections over time.

Early usage patterns reflect that goal. Collectors are insuring the pieces they actually live with. Worn regularly. Holding substantial value. Often long-term keepers. Insurance adoption by brand mirrors broader platform activity, with Rolex accounting for just over half of insured watches, followed by Omega (10%), Tudor (8%), and Cartier (7%).

It also reaches well beyond the obvious brands. Audemars Piguet, Patek Philippe, Jaeger-LeCoultre, Grand Seiko, Panerai, and a range of independent and specialist manufacturers are all represented in the insured mix, even though each represents a relatively small percentage individually. Taken together, this long tail underscores a defining reality of today’s market: meaningful value and meaningful risk exist across a wide spectrum of watches.

Insurance is meant to live inside the platform, not beside it. Alongside collection tracking and simplified resale tools, it lets collectors view their watches as a cohesive whole, rather than isolated transactions. It also lays the groundwork for what comes next, including value tracking and portfolio-level insights.

In a market where responsibility is often pushed onto the buyer and protection handled elsewhere, Bezel’s approach pulls those layers inward. Authentication, transaction, ownership, and protection now operate within a single framework, reinforcing Bezel’s role not just as a marketplace, but as a durable infrastructure for collecting done properly.

By 2025, the influence of social and celebrity culture on watch collecting was hard to miss. Wristwatches had become a default element of public presentation, present on red carpets, courtside seats, press tours, and personal announcements alike. What changed during the year was not visibility, but precision. Certain moments did more than circulate. They redirected attention, shifted demand, and, in a few cases, reshaped the hierarchy of what collectors actively sought.

One of the clearest signals came through timing rather than volume. During the Wimbledon tournament, the Rolex Datejust 41 “Wimbledon” rose quickly to become the most wanted watch on Bezel. The effect was immediate and concentrated. Interest moved in parallel with the event itself, then gradually normalized once the moment passed. A similar pattern followed Taylor Swift’s engagement announcement, where her Cartier Santos Demoiselle triggered a sudden rise in wants, inquiries, and orders. In both cases, the mechanism was simple. A familiar watch, placed into a culturally resonant moment, became newly legible to a far broader audience.

These episodes reinforced a shift already underway. Celebrity no longer functioned only as an endorsement. It had become context. The watches that moved were rarely obscure. They were recognizable references, elevated through timing and association rather than novelty.

Formal brand relationships continued to structure much of that visibility. Leonardo DiCaprio’s appointment as a Rolex Testimonee early in the year, followed by Zendaya’s later announcement, reinforced Rolex’s long-standing strategy of embedding itself in cultural authority rather than trend cycles. Jacob Elordi’s appointment as a Cartier ambassador extended the Maison’s reach to a younger, style-driven audience while preserving its foothold in classic design language.

Yet not all influence came through contracts. Timothée Chalamet remained the most instructive case. Long associated with Cartier and frequently photographed in Baignoire,Tank Mini, and Ballon Bleu references, his presence had already shaped mainstream taste. What changed in 2025 was the register. Appearances in rare Urban Jürgensen and Simon Brette pieces marked a move past brand affiliation and into collector credibility.

A parallel signal came from an unlikely source. Mark Zuckerberg, long associated with utilitarian wearables, appeared repeatedly in high-end independent and complicated references, including pieces from the likes of F.P. Journe and De Bethune. The moment mattered less for celebrity than for contrast. When a founder known for minimalism surfaced with collector-grade grails, it reframed how technical credibility and personal taste could coexist at the highest end of the market.

The effect was quiet but measurable. Interest in independent watchmaking rose not because of an announcement, but because the watches appeared in contexts that felt deliberate, consistent, and unforced.

Across the platform, the pattern repeated. Moments that mattered were rarely the loudest. They were the ones that aligned a recognizable watch with a moment of cultural permanence.

Importantly, visibility did not always translate to liquidity. Some watches spiked briefly, then receded. Others accumulated interest slowly, without headline moments, but sustained it over months. The distinction became clearer as the year progressed. Social exposure functioned less as a trigger for immediate transactions and more as a sorting mechanism. It accelerated attention toward references that were already structurally sound.

By the end of FY 2025, the landscape felt less reactive than in prior cycles. Celebrity influence remained central, but increasingly selective. Collectors appeared less interested in novelty. More attentive to continuity. Watches that moved were not those that surprised, but those that fit cleanly into an evolving picture of taste, status, and long-term relevance.

Across pricing, liquidity, and behavior, the throughline was consistency under pressure. Demand held. Engagement persisted. What changed was not appetite, but selectivity. Buyers became more deliberate. Sellers adjusted expectations. Supply constrained flow without suppressing interest. Prices normalized without unraveling.

At the same time, the year exposed how much of modern collecting now depends on expert verification rather than instinct. Rejections rose as inventory quality became more uneven. Documentation, condition, and internal integrity proved as important as brand and reference. Ownership shifted from a passive state to an actively managed one. Insurance, tracking, and verification moved from optional layers to structural necessities.

Culturally, the market continued to mature. Influence became quieter. Signals became subtler. Collectors responded less to novelty and more to continuity. Independent watchmaking gained credibility not through hype, but through context. Taste evolved not by replacement, but by refinement.

Taken together, these patterns point toward a market that is no longer driven by acceleration, but by verification, thoughtful process, and discipline. Less reactive. More intentional, and increasingly shaped by fundamentals: scarcity, replacement cost, configuration, serviceability, and long-term relevance.

Bezel’s role within that environment has shifted accordingly. No longer just a venue for transactions, the platform now operates as a system for trust, ownership, and protection.

Bezel is the top-rated marketplace for buying & selling luxury watches. We give you access to tens of thousands of the most collectible watches from the world's top professional sellers and private collectors. Every watch sold goes through our industry- leading in-house authentication process, so you can buy, sell, and bid with confidence.

Get the Bezel app on the iOS App Store or visit us at getbezel.com.

Bezel is available to download on the App Store now. Please reach out to our concierge team if there is anything we can help you with!

©2026 Bezel Inc.

All rights reserved.